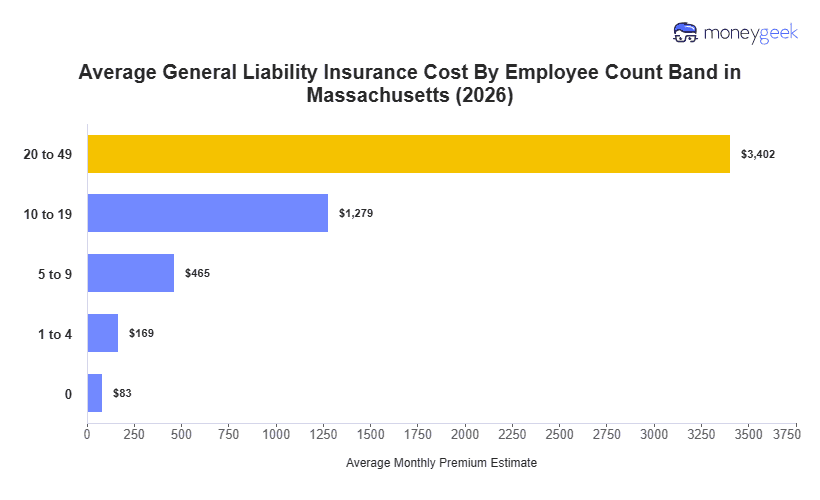

The average cost of general liability insurance in Massachusetts is $169 per month, or $2,027 annually, for businesses with one to four employees with policy limits of $1 million per occurrence/$2 million aggregate. This exceeds the national average by $46 monthly, ranking Massachusetts as the third most expensive state for general liability coverage nationwide.

The state sits at the high end of Northeast pricing. Among regional peers, only New York exceeds Massachusetts at $180 monthly, while Maine ($112), Vermont ($122), Rhode Island ($130), New Hampshire ($135) and Connecticut ($159) all come in below the state average. The spread shows a $57 gap between the lowest and highest regional costs, with Massachusetts positioned near the top of that range.

Use the state average as a reference point rather than a quote. Your actual premium depends on industry risk, business size and the coverage limits you select, all of which are factors that shift costs considerably even within Massachusetts.

A more personalized cost estimate is available through the Massachusetts general liability insurance cost calculator below.