Our analysis of Washington, D.C. professional liability insurers found three providers that consistently outperformed the rest on affordability, coverage fit and overall score.

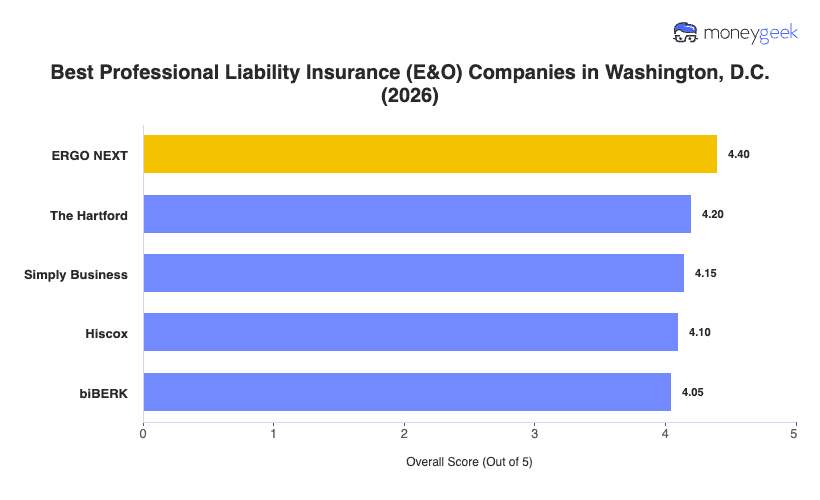

- ERGO NEXT: Ranking first across 13 of 18 industries in the district, this insurer covers more of the D.C. market's professional landscape than any other provider in the study. Its fully digital platform lets you buy a policy in about 10 minutes, manage it online around the clock and pull a certificate of insurance instantly without calling anyone. ERGO NEXT performs best for D.C. businesses in healthcare, construction, real estate, marketing, arts, fitness, pet care and cleaning services, though businesses in consulting, financial services, education and hospitality will find better-ranked options elsewhere.

- The Hartford: More than 200 years of underwriting experience shows up in the claims department, where The Hartford earns consistent marks for how it processes and pays out professional liability claims. It's the top-ranked insurer in Washington, D.C. for consultants, financial services firms, real estate professionals, educators and marketing businesses, making it a strong fit for the district's large concentration of professional services firms. D.C. healthcare providers and other professional services businesses, where The Hartford ranks ninth, are better served by another carrier on this list.

- Simply Business: Rather than underwriting policies itself, Simply Business works as a marketplace, pulling quotes from carriers including Hiscox, Travelers, Liberty Mutual and Markel so D.C. businesses can compare options in one application. That model gives it an edge for businesses that want coverage options side-by-side before committing. It ranks at the top of the D.C. market for consulting, financial services, fitness and healthcare businesses, but arts, media and recreation businesses will find stronger fits with other providers.

These three providers cover most Washington, D.C. businesses well, but no ranked list accounts for every business's specific risk profile, coverage limits or industry nuances. Comparing business insurance options directly and getting quotes from more than one carrier gives you the clearest read on what's actually right for your business.