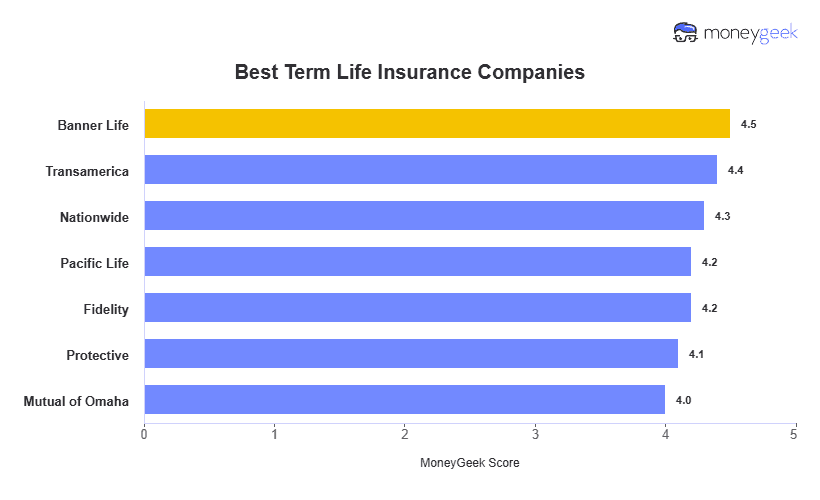

When we analyzed thousands of quotes from 25 top term life insurance companies, the most important pattern wasn't about which carrier is cheapest overall. It was about how much your age determines which carrier wins for you.

Banner Life leads for most 40-year-olds at $37 per month for women and $46 for men on a 20-year, $500,000 policy. But Fidelity's $23 monthly rate leads the field for 25-year-old women, and its pricing advantage widens to $65 or more per month for 70-year-olds.

The pricing spread between the cheapest and most expensive carrier for a 40-year-old reaches $12 per month for women, or $144 per year for identical coverage. If you're unlikely to file a claim for decades, rate leadership matters most. If you have dependents and a tight financial margin, the carrier who pays claims cleanly matters more.