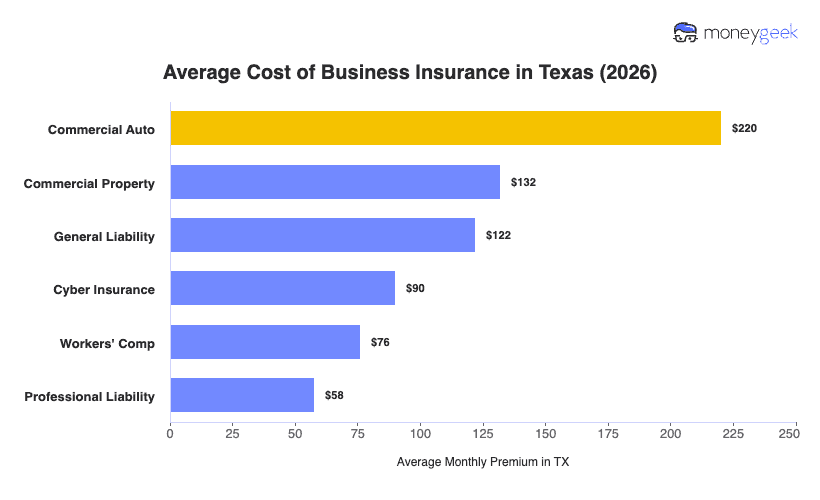

What you pay for business insurance in Texas depends on which coverages your business needs, not on a single average. Each policy is priced on its own, so your real cost is the sum of the lines you carry. The Texas average of $116 a month, or $1,396 a year, is just a blended benchmark across every industry and business size in our data, not a quote for any one business.

Say a small cleaning company signs a client contract requiring general liability and also runs a work van, so it needs commercial auto. In Texas that pairing runs about $98 per month for the general liability and $257 per month for the van, roughly $355 before anything else. A solo consultant with no vehicle or storefront would pay a fraction of that, while a contractor adding workers' comp and property coverage would pay more. Here's what each policy costs on average in Texas, what it covers and when you need it: