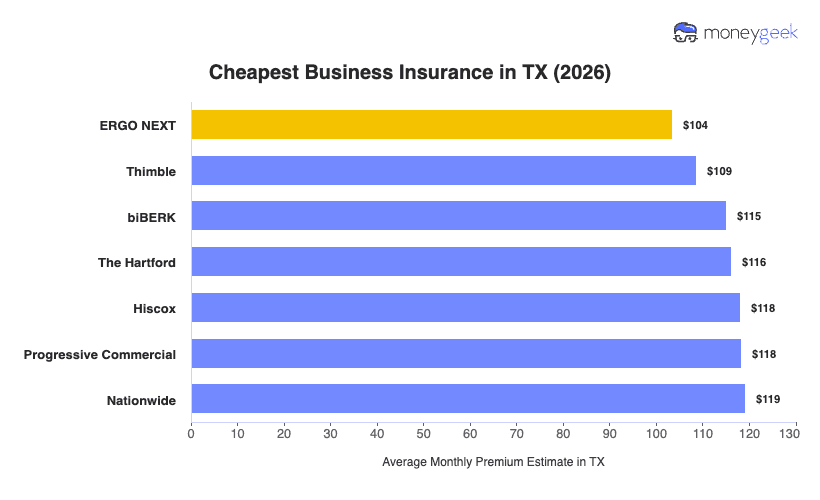

I analyzed Texas business insurance premiums across seven providers and more than 400 sub-industries, from construction and healthcare to restaurants and gyms. The cheapest insurer depends on what your business does, so I've broken my picks down by the type of business each one quotes the lowest:

- Choose If You Run a Food, Trade or Service Business: ERGO NEXT

- Choose If You Run a Fitness, Wellness or Personal-Service Business: biBerk

- Choose If You Run a Healthcare or Specialized Practice: The Hartford

- Choose If You Run a Seasonal, Event or Recreation Business: Thimble

- Choose If You Run a Professional, Consulting or Office-Based Business: Hiscox