ERGO NEXT and The Hartford tie for best small business insurance in Montana with top customer service, competitive rates and strong coverage options. ERGO NEXT ranks first in customer service and second in coverage. The Hartford ranks first in affordability and second in customer service. Simply Business offers the widest coverage selection and rounds out our top three.

Best Small Business Insurance in Montana

Get quotes from Montana's best business insurance providers, The Hartford, ERGO NEXT and Simply Business, with rates starting at $6 monthly.

Get matched to the best Montana commercial insurer for you below.

Select your industry

Select state

Updated: March 17, 2026

Advertising & Editorial Disclosure

Business Insurance in Montana: Key Takeaways

ERGO NEXT and The Hartford tie for best small business insurance in Montana, both with top customer service and comprehensive coverage.

The Hartford offers the cheapest small business insurance in Montana at $83 monthly ($998 annually).

Compare small business insurance coverage options by assessing risks, gathering quotes and bundling policies for discounts.

Get Matched to the Best Small Business Insurance Providers in Montana

Select your industry and state to get a customized quote for your Montana business.

Industry

State

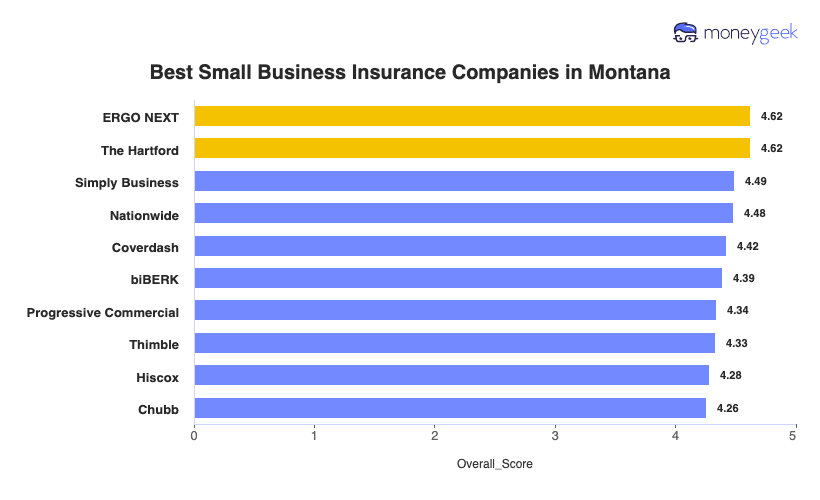

Best Small Business Insurance Companies in Montana

| ERGO NEXT | 4.62 | $100 | 1 | 2 |

| The Hartford | 4.62 | $83 | 2 | 3 |

| Simply Business | 4.49 | $97 | 5 | 1 |

| Nationwide | 4.48 | $101 | 2 | 4 |

| Coverdash | 4.42 | $100 | 6 | 2 |

| biBERK | 4.39 | $104 | 2 | 5 |

| Progressive Commercial | 4.34 | $98 | 7 | 5 |

| Thimble | 4.33 | $93 | 8 | 5 |

| Hiscox | 4.28 | $107 | 4 | 6 |

| Chubb | 4.26 | $117 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

BUSINESS INSURANCE IN MONTANA BY COVERAGE TYPE

Find the best or cheapest small business insurance in Montana for different coverage types in these resources:

ERGO NEXT

Best Montana Business Insurance

MoneyGeek Rating

4.6/ 5

4.4/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$103This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$59This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to Be Recommended to Others

4.8/5 (1st)

The Hartford

Cheapest Montana Business Insurance

MoneyGeek Rating

4.6/ 5

4.6/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$72This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$62This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

Simply Business

Best Commercial Coverage Options in Montana

MoneyGeek Rating

4.5/ 5

4.5/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$82This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$61This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

How to Get the Best Cheap Small Business Insurance in Montana

Montana has the most small business employees in the U.S., and most owners deal with wildfires and strict workers' comp thresholds. Getting small business insurance that fits these scenarios means more than shopping for low rates.

- 1

Know what Montana requires versus what your business actually needs

Montana requires workers' comp from your first employee and 25/50/20 liability for work vehicles. Meeting these requirements won't help when your Bozeman landlord demands a general liability certificate or your Billings client refuses to sign without errors and omissions coverage. You'll need coverage the state doesn't require but your contracts depend on.

- 2

Cover Montana-specific risks that standard policies miss

Montana's 2024 wildfires burned 387,966 acres across western counties, forcing business closures even without direct damage. Standard business owner's policies provide minimal business interruption protection during Missoula evacuations. Contractors need inland marine coverage to protect tools and equipment from job-site theft, a gap costing Montana businesses $15,000 to $25,000 on average.

- 3

Get quotes from Montana's top small business insurers

ERGO NEXT, The Hartford and Simply Business rank as the best small business insurance options across Montana's industries. If standard carriers turn you down due to claims history, Montana State Fund provides workers' comp as the backup option for coverage. The fund operates as both a competitive carrier and the insurer of last resort, ensuring all Montana employers can obtain required workers' comp.

- 4

Don't pick your provider based on the cheapest premium

Saving $25 monthly sounds good until Montana wildfires close your Missoula restaurant and you're waiting weeks for an adjuster while losing revenue. The 2024 fire season separated insurers who respond fast from those who leave you hanging. Ask how many adjusters each carrier maintains in Montana and typical claim resolution times before choosing the lowest price because both matter when something goes wrong.

- 5

Stack bundling and payment timing to reduce your insurance costs

Bundle general liability with property coverage into a business owner's policy to reduce what you pay across multiple policies. Pay your annual premium upfront instead of monthly to skip billing fees, which matter for Montana's seasonal tourism and hospitality businesses managing cash flow between May and September peak seasons. Claim-free discounts and safety program credits stack with these strategies to lower your business insurance costs.

- 6

Reassess coverage when your Montana business changes or expands

Opening a second location in Bozeman versus Great Falls means different insurance costs due to regional rate variations. Landing bigger contracts requiring $2 million general liability limits means increasing your coverage before you're underinsured. Add cyber liability protection if you're handling customer payment data as you grow.

Best Business Liability Insurance in Montana: Bottom Line

ERGO NEXT and The Hartford tie for Montana's best small business insurance with top customer service and comprehensive coverage. The Hartford also ranks as the cheapest option at $83 monthly. Compare quotes from both providers, assess your Montana business risks like wildfire exposure and workers' comp from your first employee, then bundle coverage to cut costs. Choose based on whether you prioritize The Hartford's low rates or ERGO NEXT's digital tools.

Business Insurance in Montana: FAQ

Small business owners in Montana often have questions about choosing the right business insurance. We answer the most common concerns below:

What business insurance do I need for my Montana business?

Montana requires workers' comp from your first employee and 25/50/20 commercial auto liability for work vehicles. Beyond legal requirements, get general liability when landlords or clients demand certificates before signing contracts. Compare quotes from ERGO NEXT, The Hartford and Simply Business to match coverage to your specific risks.

How much is small business insurance per month in Montana?

Coverage costs for your Montana business depend on your industry, claims history and employee count, but these are the monthly and annual averages by coverage type:

- General liability: $103 monthly or $1,237 annually

- Workers' compensation: $73 monthly or $878 annually

- Professional liability (E&O): $77 monthly or $926 annually

- Business owner's policy (BOP): $146 monthly or $1,758 annually

General liability vs. a BOP: which one do I need?

General liability covers customer injuries and property damage required by Montana landlords and clients. A BOP bundles general liability with commercial property. Choose general liability if you work from home with no business property, or get a BOP if you lease space or own equipment.

Do I need workers' comp in Montana if I have 1 employee (or seasonal/part-time help)?

Yes, Montana requires workers' comp from your first employee, including part-time and seasonal workers. Independent contractors need either their own coverage or an exemption certificate from Montana's Department of Labor. Contact Montana State Fund if standard carriers decline coverage due to claims history.

What do clients usually require? COI, additional insured and coverage limits?

Montana clients require certificates showing $1 million general liability per occurrence and $2 million aggregate, plus additional insured status. Professional services contracts often demand matching errors and omissions coverage. Request certificates from your insurer within 24 hours and verify additional insured endorsements appear on your policy before starting work.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.

sources

- Montana Department of Labor & Industry. "39-71-401. Employments covered and exemptions -- elections -- notice, MCA." Accessed March 25, 2026.

- Montana Department of Justice. "61-6-103. Motor vehicle liability policy minimum limits -- other requirements, MCA." Accessed March 25, 2026.

- Montana Governor's Office. "Governor Gianforte Praises DNRC for 2024 Fire Season Response." Accessed March 25, 2026.

- Montana State Fund. "Who is Covered." Accessed March 25, 2026.

- U.S. Small Business Administration Office of Advocacy. "2024 Small Business Profile: Montana." Accessed March 25, 2026.