ERGO NEXT leads our Maryland business insurance analysis with excellent customer service, competitive rates and comprehensive coverage. The Hartford and Simply Business are also strong choices for business owners in the Old Line State.

Best Small Business Insurance in Maryland

Get quotes from Maryland's best business insurance providers, ERGO NEXT, The Hartford and Simply Business, with rates starting at $6 monthly.

Get matched to the best Maryland commercial insurer for you below.

Select your industry

Select state

Updated: March 17, 2026

Advertising & Editorial Disclosure

Business Insurance in Maryland: Key Takeaways

ERGO NEXT offers Maryland's best small business insurance with top customer service scores and comprehensive coverage ranking second.

The Hartford offers the cheapest small business insurance in Maryland at $80 monthly ($959 annually).

Finding the right small business insurance coverage means assessing your risks, comparing quotes and using available discounts.

Get Matched to the Best Small Business Insurance Providers in Maryland

Select your industry and state to get a customized quote for your Maryland business.

Industry

State

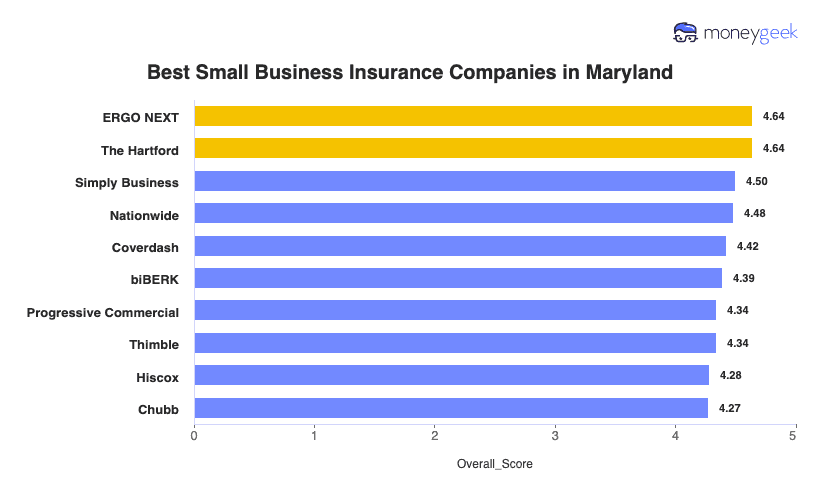

Best Small Business Insurance Companies in Maryland

| ERGO NEXT | 4.64 | $95 | 1 | 2 |

| The Hartford | 4.64 | $80 | 2 | 3 |

| Simply Business | 4.50 | $92 | 5 | 1 |

| Nationwide | 4.48 | $96 | 2 | 4 |

| Coverdash | 4.42 | $96 | 6 | 2 |

| biBERK | 4.39 | $100 | 2 | 5 |

| Progressive Commercial | 4.34 | $95 | 7 | 5 |

| Thimble | 4.34 | $89 | 8 | 5 |

| Hiscox | 4.28 | $103 | 4 | 6 |

| Chubb | 4.27 | $112 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

RESEARCH THE BEST BUSINESS INSURANCE IN MARYLAND BY COVERAGE TYPE

Discover the best or cheapest business insurer in Maryland for your desired coverage type in our resources below:

ERGO NEXT

Best Maryland Business Insurance

MoneyGeek Rating

4.6/ 5

4.5/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$98This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$66This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to Be Recommended to Others

4.8/5 (1st)

The Hartford

Cheapest Maryland Business Insurance

MoneyGeek Rating

4.6/ 5

4.6/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$78This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$67This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

Simply Business

Best Commercial Coverage Options in Maryland

MoneyGeek Rating

4.5/ 5

4.5/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$78This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$67This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

How to Get the Best Cheap Small Business Insurance in Maryland

Maryland small business owners deal with Chesapeake Bay flooding, brutal winter storms and some of the strictest workers' comp rules in the country. Getting business insurance that covers these risks takes more than shopping for the lowest price.

- 1

Know what Maryland law requires versus what protects your business

Maryland law requires workers' compensation from your first hire, 30/60/15 liability minimums for work vehicles and $50,000 in general liability for licensed contractors. Cover what the law requires, then add what your business actually needs, like professional liability coverage, which isn't state-mandated but most clients require before they sign commercial contracts.

- 2

Address hazards unique to your Maryland operation

Chesapeake Bay flooding hit Baltimore and Annapolis with 12 and 11 high-tide flood days in 2023 and standard commercial property policies exclude flood damage entirely. Small businesses with business interruption coverage stay financially stable when winter ice storms force closures across the Baltimore-Washington corridor, covering lost revenue while you can't operate. Without these coverage types, you absorb losses that could bankrupt a small operation.

- 3

Don't skip Maryland's assigned risk option when shopping rates

Start with ERGO NEXT, The Hartford and Simply Business for standard market quotes. If carriers reject you because of high-risk operations or past claims, Chesapeake Employers' Insurance provides workers' compensation through Maryland's assigned risk pool. Expect premiums 25% to 50% higher than standard rates, but coverage beats the penalties Maryland imposes for operating uninsured (fines start at $1,000 and climb fast).

- 4

Don't make low premiums your only priority

The cheapest Maryland business insurance won't help if it takes weeks to process claims. The 2024 winter ice storms separated responsive carriers from slow ones across the Baltimore-Washington corridor. Ask providers about their Maryland adjuster count and claim resolution times, as both deliver value when you need it the most.

- 5

Stack bundling discounts with Maryland safety incentives

Bundle general liability with commercial property in a business owner's policy cuts your combined premiums 20% to 30%. Pay your full annual premium upfront instead of monthly to avoid $200 to $400 in installment fees. Maryland insurers reward claim-free years and safety training completion, and these discounts compound when you stack them together over time.

- 6

Reassess your policies after Maryland growth milestones

Maryland's one-employee workers' compensation threshold triggers mandatory coverage when you hire. Expanding from Baltimore to the Eastern Shore means different premium rates, since Montgomery County businesses pay 18% to 32% more than rural areas. Landing contracts with federal agencies often requires $2 million aggregate limits. Review your business insurance costs before growth happens, not after you're already committed and exposed.

Best Business Liability Insurance in Maryland: Bottom Line

ERGO NEXT leads Maryland with top customer service and comprehensive coverage, while The Hartford offers the most affordable rates at $80 monthly. Compare quotes, assess your risks and use available discounts to find the right coverage for your business.

Business Insurance in Maryland: FAQ

Small business owners in Maryland often have questions about choosing the right business insurance. We answer the most common concerns below:

What insurance do I need for my small business in Maryland?

Maryland law requires workers' compensation from your first hire, 30/60/15 commercial auto minimums for work vehicles and $50,000 in general liability for licensed contractors. Add professional liability when clients demand proof before signing contracts, and consider business interruption coverage if winter storms or Chesapeake Bay flooding could shut down your operation.

How much does small business insurance cost in Maryland?

Coverage costs for your Maryland business depend on your industry, but these are the monthly and annual averages by coverage type:

- General liability: $99 monthly or $1,185 annually

- Workers' compensation: $70 monthly or $842 annually

- Professional liability (E&O): $74 monthly or $889 annually

- Business owner's policy (BOP): $140 monthly or $1,686 annually

What should I buy first: general liability, a BOP, workers' comp or professional liability?

Start with what Maryland law mandates: workers' compensation if you have employees and commercial auto if you use work vehicles. If neither applies, buy general liability first since Baltimore landlords and clients demand it before signing leases or contracts. Add a BOP when you need both general liability and property coverage together.

Who has the best small business insurance in Maryland?

ERGO NEXT leads Maryland with top customer service scores and comprehensive coverage options ranking second overall. The Hartford offers the most affordable rates at $80 monthly while maintaining strong claims service. Simply Business provides the broadest coverage selection, ranking first for policy options. Your best choice depends on whether you prioritize service, cost or coverage variety.

How do I get a COI fast, and what does "additional insured" mean?

Choose insurers like ERGO NEXT that issue certificates of insurance instantly through their online platforms, like waiting days for paperwork costs you deals. "Additional insured" extends your liability coverage to protect your client or landlord when they're named on your policy. Request this endorsement when signing contracts or leases requiring proof of insurance.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.