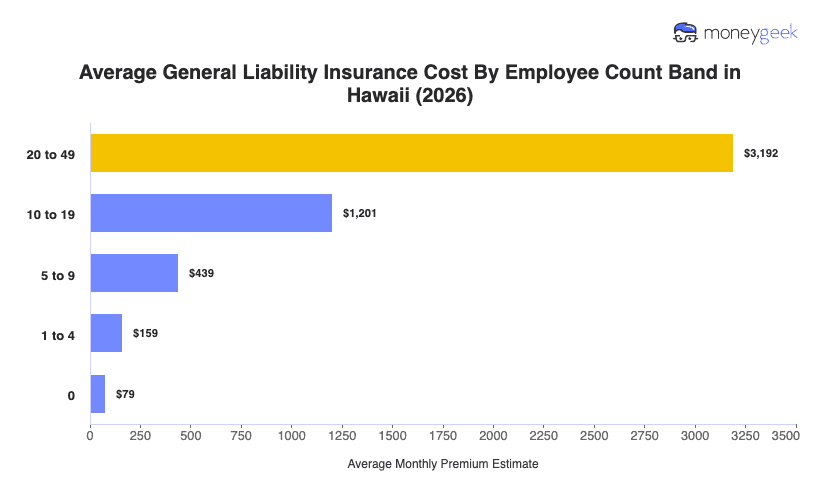

The average cost of general liability insurance nationally runs $123 per month for businesses with one to four employees. Hawaii's benchmark sits at $159 per month or $1,913 per year, about 30% above that figure, placing the state 46th in affordability out of 50 states and the District of Columbia.

Hawaii isn't an outlier within its region, it's the norm. Every Pacific state is above the national average, ranging from $138 in Oregon to $190 in California, with Alaska, Washington and Hawaii grouped in the $151 to $159 range. Geographic isolation, a higher cost of doing business and a less competitive insurance market likely account for Hawaii's position within that elevated range.

Hawaii's figure is a state average, not a rate prediction. The more useful question isn't how close your quote lands to that number, it's what's driving your cost in the first place. A more personalized cost estimate is available through the Hawaii general liability insurance cost calculator below.