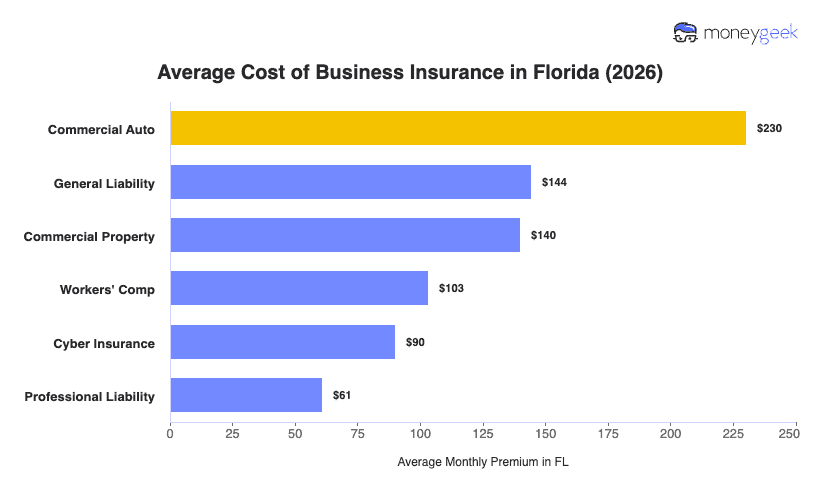

The cost of business insurance in Florida is $128 per month on average, or $1,538 a year. That figure is a composite average across all six coverage types, 25 industries and every business size in our data, so treat it as a benchmark for comparison, not a quote for your own business. What you actually pay depends on which coverages you carry and the limits you set on each.

Two of those coverages scale with the size of your operation instead of sitting at a flat rate. Workers' compensation is priced per employee, so it climbs as you add staff, and commercial auto is priced per vehicle, so a business running a fleet pays far more than one with a single van. The rest are quoted as flat monthly averages. Here's what each policy costs in Florida, what it covers and when your business needs it.