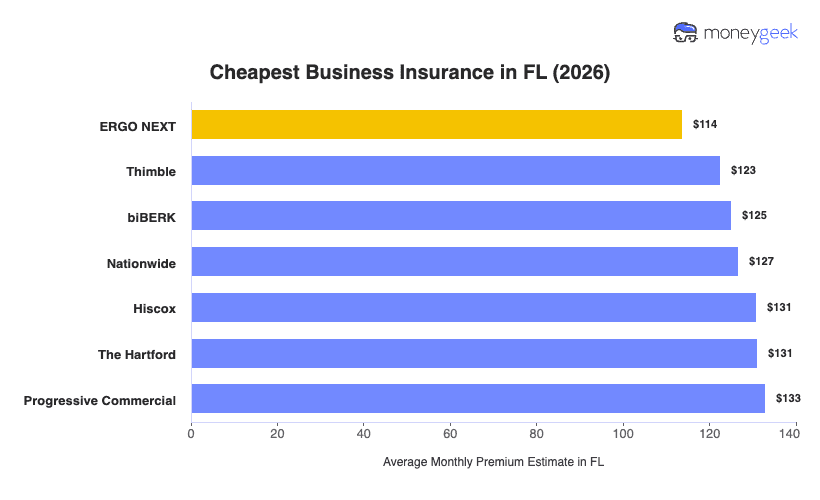

ERGO NEXT, Thimble and biBerk are the three cheapest business insurance providers in Florida in my analysis, all priced below the state average of $128 per month:

- ERGO NEXT: Averages about $114 per month, roughly 11% below the state average. It is the cheapest analyzed carrier in six of Florida's 25 industry groups, including construction and contracting and food and beverage, and it prices lowest for professional liability.

- Thimble: Averages about $123 per month, around 4% below the state average. Its overall rate sits mid-pack, but it is the cheapest option for a set of specific trades, such as ambulance services and woodworking.

- biBerk: Averages about $125 per month, close to 1% below the state average. It prices lowest in fitness services, beauty and wellness, and marketing and communications.

These rankings come from standardized sample profiles, so your actual cost will vary with your business's specifics.