MoneyGeek analyzed average monthly rates across vehicle types and industries to identify the cheapest commercial auto insurers in Pennsylvania.

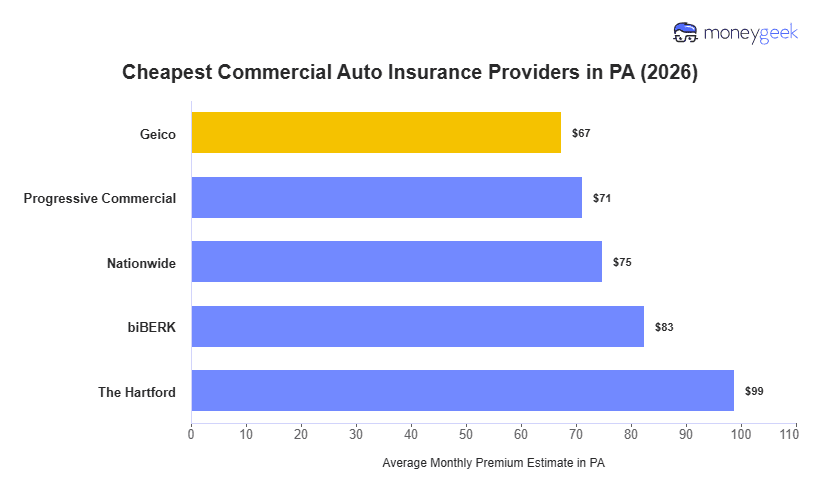

- GEICO averages $67 per month for commercial auto insurance in Pennsylvania, 15% below the state average. It prices lowest across 15 of 25 general industries in MoneyGeek's Pennsylvania analysis, with its strongest savings for office-based businesses, financial services and wellness-sector companies. Pennsylvania businesses in financial services see GEICO's deepest savings at 26% below the industry average.

- Progressive Commercial averages $71 per month, 10% below the Pennsylvania state average. It ranks first in affordability for 10 general industries in MoneyGeek's Pennsylvania analysis, including wholesale and distribution, transportation and logistics, childcare services and manufacturing. Pennsylvania businesses in wholesale and distribution see Progressive Commercial's strongest savings at 31% below the industry average.

- Nationwide averages $75 per month, 5% below the Pennsylvania state average. It's the third-cheapest option overall in MoneyGeek's Pennsylvania analysis and a reasonable fit for businesses that don't fall squarely into the industry profiles where GEICO or Progressive Commercial price lowest.

Pennsylvania commercial auto insurance costs vary by vehicle fleet details, driver records, services offered and location within the state, so these rankings won't apply uniformly to every Pennsylvania business. Use these companies as a starting point when comparing Pennsylvania commercial auto insurance costs to get the lowest-cost policy that meets your needs.