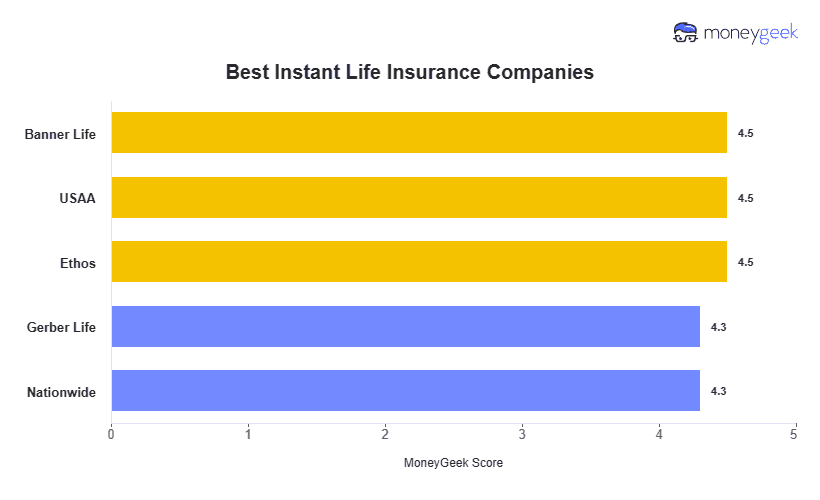

Banner Life, USAA, Ethos, Gerber Life and Nationwide are our top picks for the best online instant life insurance companies in 2026. Max coverage limits for instant policies range from $1 million with Gerber Life to $10 million with USAA, and all five carriers in our list hold AM Best financial strength ratings of A+ or higher. USAA offers the highest instant coverage limit at $10 million across both term and whole life, while Ethos is the only provider on the list with four instant policy types, including indexed universal life and final expense coverage.

Coverage limit and policy type are the biggest differentiators in our analysis. If you need more than $5 million in instant coverage, USAA is the only option. If you want a fully digital process with no agent call, Ethos and Nationwide are the two carriers that deliver that experience. Banner Life wins on term affordability but requires a brief agent conversation for final approval.