ERGO NEXT leads MoneyGeek's study as the best small business insurance in Utah with top scores in customer service and coverage. The Hartford offers the lowest rates at $85 monthly, while Simply Business provides the broadest coverage options for Utah small business owners.

Best Small Business Insurance in Utah

Get quotes from Utah's best business insurance providers, ERGO NEXT, The Hartford and Simply Business, with rates starting at $69 annually.

Get matched to the best Utah commercial insurer for you below.

Select your industry

Select state

Updated: March 20, 2026

Advertising & Editorial Disclosure

Business Insurance in Utah: Key Takeaways

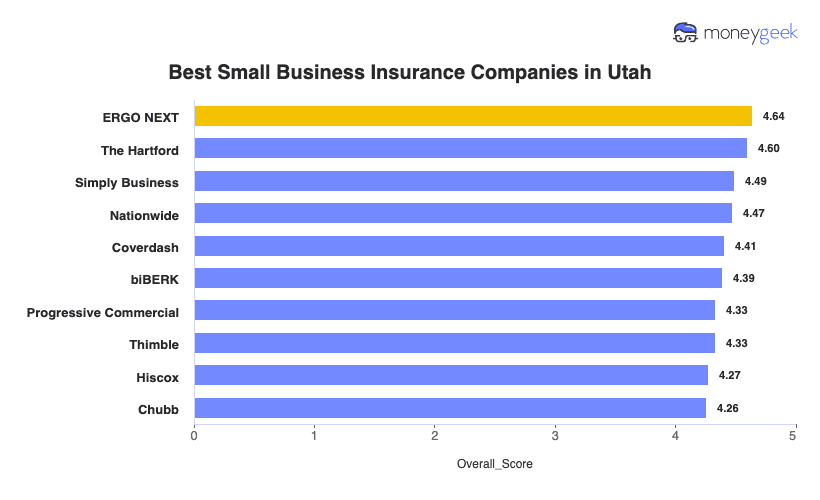

ERGO NEXT ranks as the best small business insurance in Utah, leading in customer service and coverage.

The Hartford offers the cheapest small business insurance in Utah at $85 monthly ($1,021 annually).

Compare quotes and bundle small business insurance coverage to match your risks and save on premiums.

Best Small Business Insurance Companies in Utah

| ERGO NEXT | 4.64 | $86 | 1 | 2 |

| The Hartford | 4.60 | $85 | 2 | 3 |

| Simply Business | 4.49 | $93 | 5 | 1 |

| Nationwide | 4.47 | $97 | 2 | 4 |

| Coverdash | 4.41 | $96 | 6 | 2 |

| biBERK | 4.39 | $100 | 2 | 5 |

| Progressive Commercial | 4.33 | $94 | 7 | 5 |

| Thimble | 4.33 | $90 | 8 | 5 |

| Hiscox | 4.27 | $103 | 4 | 6 |

| Chubb | 4.26 | $112 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

FIND THE BEST BUSINESS INSURANCE IN UTAH BY COVERAGE TYPE

Find the best and cheapest small business insurance providers in Utah for general liability, workers' comp, professional liability and more:

ERGO NEXT

Best Utah Business Insurance

MoneyGeek Rating

4.6/ 5

4.5/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$84This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$66This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to Be Recommended to Others

4.8/5 (1st)

The Hartford

Cheapest Utah Business Insurance

MoneyGeek Rating

4.6/ 5

4.5/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$86This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$66This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

Simply Business

Best Commercial Coverage Options in Utah

MoneyGeek Rating

4.5/ 5

4.5/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$92This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$68This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

Get Matched to the Best Small Business Insurance Providers in Utah

Select your industry and state to get a customized quote for your Utah business.

Industry

State

How to Get the Best Cheap Small Business Insurance in Utah

Utah small business owners, from Wasatch Front contractors to Salt Lake City restaurants to Provo tech startups, have risks like earthquakes and spring flooding from snowmelt. Getting business insurance that covers these hazards takes more than finding the cheapest premium.

- 1

Know Utah legal requirements and actual protection needs

Utah law requires workers' compensation from your first employee, commercial auto liability at $30,000/$65,000/$25,000 (increased January 1, 2025), and $3,000 minimum PIP coverage. Contractors need $100,000/$300,000 general liability to maintain DOPL licenses. Beyond legal mandates, landlords require commercial property coverage, and lenders mandate flood insurance for properties in the 186+ NFIP participating communities when you have a federally backed mortgage.

- 2

Match coverage to Utah industry and regional risks

Earthquake coverage protects restaurant equipment, retail inventory, and office technology from non-structural damage that standard policies exclude. Utah's Wasatch Front sits on major fault lines. Professional liability covers consultants and tech firms when clients claim your advice caused financial losses. Cyber liability protects businesses storing customer data, which matters more given Utah's competitive hiring market where data breaches hurt recruitment and retention.

- 3

Get quotes from top carriers and Utah programs

Since Utah doesn't maintain state workers' comp funds or assigned risk pools, compare private market carriers to find competitive rates. The difference between The Hartford and Chubb reaches $324 annually. Savings from getting better rates means more funds for other business needs.

- 4

Look beyond the cheapest monthly premium

The cheapest policy won't help when spring flooding hits and you discover it excludes earthquake damage Utah businesses need. Consider providers that offer specialized options (pollution liability for contractors, product liability for food retailers, liquor liability for restaurants), have excellent customer service and processes claims efficiently. Check AM Best ratings (A- or higher) and ask about response times for COI requests, which most Utah businesses need.

- 5

Stack bundling discounts with payment strategies for lower rates

Business insurance costs add up quickly when covering multiple risks. Bundle general liability with commercial property in a business owner's policy to cut combined premiums 20% to 30%, then add workers' comp and commercial auto for additional multi-policy discounts. Pay annually instead of monthly to avoid $200 to $400 in installment fees, and ask Utah insurers about claim-free discounts and safety program credits.

- 6

Update coverage as your Utah business evolves

Landing contracts above $1 million requires commercial umbrella coverage when your general liability limits won't cover large claims. Storing customer property in your warehouse requires bailee coverage, whether you're holding equipment for repairs or inventory awaiting distribution. Start manufacturing or selling products and you need product liability, from craft goods in Provo workshops to retail merchandise in Park City shops.

Best Business Liability Insurance in Utah: Bottom Line

ERGO NEXT leads Utah in customer service and coverage. The Hartford offers the most affordable option at $85 monthly. Compare quotes from both carriers and bundle coverages for earthquake, flood and workers' comp protection to cut premiums 20% to 30%.

Business Insurance in Utah: FAQ

Small business owners in Utah often have questions about choosing the right business insurance. We answer the most common concerns below:

What insurance do I need to start a small business in Utah?

Utah requires workers' compensation from your first employee and commercial auto liability of $30,000/$65,000/$25,000 if you drive for business. Contractors need $100,000/$300,000 general liability for DOPL licenses. Add earthquake and flood coverage to protect against Utah-specific financial risks.

How much does small business insurance cost per month in Utah for my type of business?

Coverage costs for your Utah business depend on your industry, but here are the monthly and annual averages by coverage type:

- General liability: $98 monthly or $1,179 annually

- Workers' compensation: $70 monthly or $843 annually

- Professional liability (E&O): $74 monthly or $889 annually

- Business owner's policy (BOP): $139 monthly or $1,673 annually

What's required in Utah vs what my client, landlord or venue requires for a COI?

Utah requires workers' comp for one employee and commercial auto for business driving. Contractors need $100,000/$300,000 general liability for DOPL licenses. Clients, landlords and venues require higher limits, additional insured status and commercial property coverage beyond state minimums.

How fast can I get proof of insurance (COI) and add my client as additional insured?

ERGO NEXT and The Hartford issue certificates of insurance within 24 hours after purchase. You'll add clients as additional insureds during the quote process or by contacting your agent afterward. Digital carriers like ERGO NEXT often provide instant COI downloads.

Will it cover common claims like customer injuries, property damage, employee injuries or business driving?

General liability covers customer injuries and property damage you cause. Workers' compensation covers employee injuries. Commercial auto covers business driving accidents. Bundle these coverages with commercial property in a business owner's policy for most common Utah claims.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.

sources

- Utah Division of Professional Licensing. "Specialty Contractor License Requirements." Accessed March 24, 2026.

- Utah Labor Commission. "Employers' Guide to Workers' Compensation." Accessed March 24, 2026.

- Utah Legislature. "H.B. 113 Motor Vehicle Insurance Revisions, Enrolled Copy." Accessed March 24, 2026.