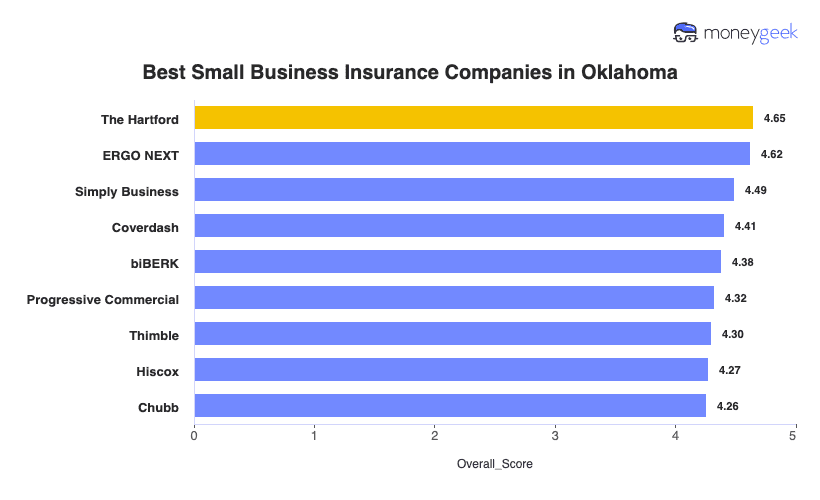

The Hartford leads Oklahoma small business insurance with top rankings in affordability and financial strength. It offers the lowest rates statewide at $83 monthly while maintaining an A+ AM Best rating. ERGO NEXT and Simply Business also provide strong coverage options for Oklahoma business owners.

Best Small Business Insurance in Oklahoma

Get quotes from Oklahoma's best business insurance providers, The Hartford, ERGO NEXT and Simply Business, with rates starting at $6 monthly.

Get matched to the best Oklahoma commercial insurer for you below.

Select your industry

Select state

Updated: March 16, 2026

Advertising & Editorial Disclosure

Business Insurance in Oklahoma: Key Takeaways

Oklahoma's best small business insurance comes from The Hartford, which ranks first in affordability and financial strength statewide.

The Hartford, Simply Business and Thimble have the cheapest small business insurance rates for small business owners in Oklahoma, starting at $83 monthly.

To choose the right small business insurance coverage, assess your risks, compare quotes from multiple providers and claim all discounts.

Best Small Business Insurance Companies in Oklahoma

| The Hartford | 4.65 | $83 | 2 | 3 |

| ERGO NEXT | 4.62 | $94 | 1 | 2 |

| Simply Business | 4.49 | $84 | 5 | 1 |

| Coverdash | 4.41 | $95 | 6 | 2 |

| biBERK | 4.38 | $98 | 2 | 5 |

| Progressive Commercial | 4.32 | $93 | 7 | 5 |

| Thimble | 4.30 | $89 | 8 | 5 |

| Hiscox | 4.27 | $102 | 4 | 6 |

| Chubb | 4.26 | $111 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

FIND THE BEST BUSINESS INSURANCE IN OKLAHOMA BY COVERAGE TYPE

The best or cheapest business insurer in Oklahoma varies depending on what coverage type you need. Read our resources to find what matches your business:

The Hartford

Best and Cheapest Oklahoma Business Insurance

MoneyGeek Rating

4.7/ 5

4.7/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$85Rates shown for small businesses with two employees across 79 industries. General liability policies only.Average Monthly Cost of Workers' Comp Insurance

$65Rates shown for small businesses with two employees across 79 industries. Workers' comp policies only.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

ERGO NEXT

Best Oklahoma Customer Experience

MoneyGeek Rating

4.6/ 5

4.4/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$97This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$65This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to Be Recommended to Others

4.8/5 (1st)

Simply Business

Best Commercial Coverage Options in Oklahoma

MoneyGeek Rating

4.5/ 5

4.4/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$80This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$66This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

Get Matched to the Best Small Business Insurance Providers in Oklahoma

Select your industry and state to get a customized quote for your Oklahoma business.

Industry

State

How to Get the Best Cheap Small Business Insurance in Oklahoma

Oklahoma requires workers' compensation from your first employee and commercial auto for work vehicles, but meeting legal minimums won't protect you when clients demand liability certificates or severe weather closes operations. Getting business insurance means covering gaps between state requirements and business reality.

- 1

Know Oklahoma legal requirements and coverage gaps

Oklahoma requires workers' compensation from your first employee (no exemptions unless you only employ family) and 25/50/20 commercial auto liability if employees drive for work. Meeting these won't help when clients refuse contracts without professional liability, landlords demand general liability certificates or you need customer injury coverage, since these protect your business even though state law doesn't mandate them.

- 2

Address hazards specific to your Oklahoma operation

Oklahoma's 152 tornadoes in 2024 threaten property-heavy businesses with closures. Contractors need inland marine covering tools stolen from job sites. Professional services need errors and omissions protection when advice causes client financial losses. Oklahoma City restaurants serving alcohol must carry liquor liability since ABLE certificates require coverage proof. Delivery businesses need hired and non-owned auto beyond basic commercial policies.

- 3

Get quotes from top carriers and Oklahoma's backup option

Oklahoma's top providers offer affordable rates and broad coverage for local businesses: The Hartford averages $83 monthly while ERGO NEXT costs $94 monthly, both maintaining A-rated financial strength. If standard carriers decline your application because of claims history or your industry, CompSource Mutual provides Oklahoma's workers' compensation backup coverage, ensuring you meet the state's mandatory requirement when private insurers refuse.

- 4

Balance affordability with service quality and coverage fit

Saving $20 monthly backfires when your cheapest policy excludes coverage clients require or takes three weeks to issue certificates while contractors need them within 48 hours for job starts. ERGO NEXT ranks first for customer service with instant certificate generation, while The Hartford's A+ financial rating means reliable claim payment when Oklahoma storms damage property. Ask providers about certificate turnaround times, coverage options for your industry and claims response speeds.

- 5

Stack bundling with Oklahoma safety program discounts

Bundle general liability with commercial property into a business owner's policy to cut combined premiums 20% to 30%. That's important savings since Oklahoma businesses face tornado, hail and earthquake property risks. Pay annually instead of monthly to avoid $200 to $400 in billing fees. Enroll in Oklahoma's Workers' Compensation Premium Reduction program for safety training discounts, reducing your cost of business insurance across policies.

- 6

Reassess coverage when your Oklahoma business grows

Opening a second location in Tulsa versus rural counties changes property insurance costs because tornado frequency varies by region. Oklahoma's 371,640 small businesses pay different rates based on geography. Landing larger contracts requiring $2 million general liability limits instead of $1 million means updating coverage before project work starts. Adding cyber liability when you start processing customer credit cards or hiring employees who drive company vehicles both demand coverage reassessment.

Best Business Liability Insurance in Oklahoma: Bottom Line

The Hartford ranks first for Oklahoma small business insurance and has the lowest rates at $83 monthly. Simply Business and Thimble also offer competitive pricing. Compare quotes from these providers, assess your tornado and workers' comp risks for Oklahoma operations and stack bundling discounts with safety program credits to cut costs.

Business Insurance in Oklahoma: FAQ

Small business owners in Oklahoma often have questions about choosing the right business insurance. We answer the most common concerns below:

What insurance do I need to start a small business in Oklahoma?

Oklahoma requires workers' compensation from your first employee and 25/50/20 commercial auto liability if employees drive for work. You'll also need general liability for landlord requirements and professional liability if clients demand it before signing contracts, even though state law doesn't mandate these coverages.

What does Oklahoma require vs what a landlord, client or venue will ask for?

Oklahoma law requires workers' comp from your first employee and commercial auto for work vehicles. Landlords demand general liability certificates before lease signing. Clients refuse contracts without professional liability coverage. Venues require liquor liability for events serving alcohol, none of which state law mandates for your business.

How much does small business insurance cost per month in Oklahoma?

Coverage costs for your Oklahoma business depend on your industry, but these are the monthly and annual averages by coverage type:

- General liability: $98 monthly or $1,178 annually

- Workers' compensation: $69 monthly or $823 annually

- Professional liability (E&O): $73 monthly or $877 annually

- Business owner's policy (BOP): $138 monthly or $1,656 annually

Can I get a COI fast for a job, lease or event, and what do I need to provide?

ERGO NEXT provides instant certificates through its mobile app 24/7 at no extra cost. You'll need your policy number, coverage limits, effective dates and the certificate holder's name and address. The Hartford and Simply Business issue certificates within one to three business days after you request them.

Do I need workers' comp if I hire my first employee (or use 1099s), and what if I drive my personal car for work?

Yes, Oklahoma requires workers' compensation from your first employee with no exemptions unless you only employ family members. Independent contractors don't trigger this requirement because they're not your employees. Driving your personal car for work needs hired and non-owned auto coverage beyond your personal policy.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.

sources

- Oklahoma ABLE Commission. "Frequently Asked Questions." Accessed March 25, 2026.

- Oklahoma Department of Emergency Management. "Tornadoes." Accessed March 25, 2026.

- Oklahoma Insurance Department. "FAQs." Accessed March 25, 2026.

- Oklahoma Workers' Compensation Court of Existing Claims. "Employers FAQ." Accessed March 25, 2026.

- U.S. Small Business Administration Office of Advocacy. "2023 Small Business Economic Profile - Oklahoma." Accessed March 25, 2026.