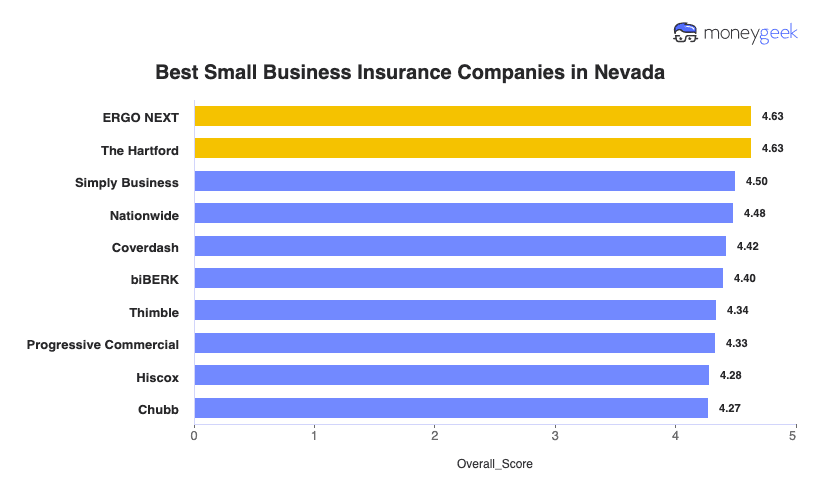

ERGO NEXT and The Hartford tie for Nevada's best small business insurance with top customer service and competitive rates at $102 monthly. Simply Business ranks third, offering strong coverage options through its multi-carrier marketplace for Nevada small business owners.

Best Small Business Insurance in Nevada

Get quotes from Nevada's best business insurance providers, ERGO NEXT, The Hartford and Simply Business, with rates starting at $7 monthly.

Get matched to the best Nevada commercial insurer for you below.

Select your industry

Select state

Updated: March 17, 2026

Advertising & Editorial Disclosure

Business Insurance in Nevada: Key Takeaways

ERGO NEXT and The Hartford tie for best small business insurance in Nevada with 4.63 MoneyGeek scores, excelling in service and affordability.

The Hartford offers the cheapest small business insurance in Nevada at $102 monthly or $1,222 annually.

Compare quotes from multiple insurers for small business insurance coverage, assess your risks and stack available discounts.

Best Small Business Insurance Companies in Nevada

| ERGO NEXT | 4.63 | $102 | 1 | 2 |

| The Hartford | 4.63 | $102 | 2 | 3 |

| Simply Business | 4.50 | $110 | 5 | 1 |

| Nationwide | 4.48 | $116 | 2 | 4 |

| Coverdash | 4.42 | $115 | 6 | 2 |

| biBERK | 4.40 | $119 | 2 | 5 |

| Thimble | 4.34 | $107 | 8 | 5 |

| Progressive Commercial | 4.33 | $113 | 7 | 5 |

| Hiscox | 4.28 | $122 | 4 | 6 |

| Chubb | 4.27 | $134 | 3 | 4 |

Note: These rates reflect MoneyGeek's analysis of small businesses with two employees across 79 major industries. Your actual rates vary based on your industry risk factors, claims history, coverage limits and individual insurer underwriting criteria. Contact insurers directly for personalized quotes.

BEST BUSINESS INSURANCE IN NEVADA BY COVERAGE TYPE

Find the best or cheapest small business insurer in Nevada for your coverage type in the resources below:

The Hartford

Best and Cheapest Nevada Business Insurance

MoneyGeek Rating

4.6/ 5

4.6/5Affordability

4.6/5Customer Experience

4.7/5Coverage Options

Average Monthly Cost of General Liability Insurance

$103This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$79This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Claims Process

4.5/5 (1st)Our Survey: Agent Service

4.7/5 (1st)

ERGO NEXT

Best Nevada Customer Experience

MoneyGeek Rating

4.6/ 5

4.5/5Affordability

4.7/5Customer Experience

4.8/5Coverage Options

Average Monthly Cost of General Liability Insurance

$100This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$78This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Survey: Digital Experience

4.8/5 (1st)Our Survey: Likely to be Recommended to Others

4.8/5 (1st)

Simply Business

Best Commercial Coverage Options in Nevada

MoneyGeek Rating

4.5/ 5

4.5/5Affordability

4.2/5Customer Experience

4.9/5Coverage Options

Average Monthly Cost of General Liability Insurance

$109This rate is for small businesses with two employees across 79 major industries or business types and focus solely on general liability policies.Average Monthly Cost of Workers' Comp Insurance

$81This rate is for small businesses with two employees across 79 major industries or business types and focus solely on workers' comp policies.Our Research: Digital Experience

4.5/5Our Survey: Service Quality

4.0/5

Get Matched to the Best Small Business Insurance Providers in Nevada

Select your industry and state to get a customized quote for your Nevada business.

Industry

State

How to Get the Best Cheap Small Business Insurance in Nevada

Nevada business owners face wildfire seasons forcing operational shutdowns, unexpected desert flooding and contractor liability rules stricter than neighboring states. Learning how to get business insurance in Nevada means addressing coverage gaps that price shopping alone won't solve.

- 1

Know what Nevada law requires versus what contracts demand

Nevada requires 25/50/20 auto liability for company vehicles and workers' comp from your first hire. Meeting state minimums won't land contracts. Reno casinos demand $2 million in general liability before contractors start work. Las Vegas landlords require insurance certificates before signing commercial leases. Henderson tech companies need cyber liability for client data. Neither of these are legally required, but you'll need them to get business.

- 2

Address threats your Nevada small business actually encounters

Nevada's 108 wildfires in 2024 burned 69,258 acres, yet small businesses in Tahoe Basin and Elko County have difficulty obtaining wildfire coverage since some insurers stopped accepting applications in high-risk zones. Flood disasters show commercial property policies exclude Nevada's water risks. Tools and equipment insurance protects contractor gear from Las Vegas construction site theft, where losses average $15,000 to $25,000 per incident.

- 3

Compare top carriers and Nevada State Fund rates

We analyzed ERGO NEXT, The Hartford, and Simply Business for Nevada rankings. The Hartford offers the lowest rates at $83 monthly for general liability, which is important when 35% of Nevada owners adapt to inflation and 25% say funding access is their top challenge. Nevada State Fund provides workers' comp when private carriers reject high-risk businesses. Rural Nevada companies may find fewer carrier options than Las Vegas or Reno counterparts.

- 4

Don't sacrifice claim speed for monthly savings (58 words)

Saving $25 monthly matters when 47% of Nevada businesses struggle with finding customers and budgets are tight. But 2024's wildfires proved cheap coverage fails when carriers take weeks assigning adjusters while Sparks warehouses sit closed. Lost revenue from slow claims erases years of premium savings. Ask carriers about Nevada adjuster count and resolution timeframes before choosing the lowest rate.

- 5

Use bundling and discounts to offset Nevada insurance costs

Bundle liability and property into business owner's policies to cut business insurance costs by 20% to 30%. That's substantial savings for startups with funding challenges and established companies managing inflation pressure. Pay annually to eliminate monthly billing fees. Safety certifications, security systems and claim-free histories stack additional discounts. These savings help protect Nevada businesses in the state's tax-friendly environment without straining cash flow.

- 6

Update coverage when your Nevada operations expand

Thirty-one percent of Nevada businesses say managing growth is challenging. Growth creates coverage gaps: opening Reno locations after starting in Las Vegas, hiring your first employee requiring immediate workers' comp or landing contracts demanding higher liability limits. Adding vehicles, equipment or leased space all need policy updates before incidents expose vulnerabilities.

Best Business Liability Insurance in Nevada: Bottom Line

ERGO NEXT and The Hartford both scored 4.63 in MoneyGeek's analysis of Nevada small business insurance. The Hartford offers the lowest rates at $102 monthly, making it best for budget-conscious owners. Compare quotes from ERGO NEXT and The Hartford, assess your wildfire and flood exposure, then bundle coverage to stack discounts. Choose The Hartford for affordability or ERGO NEXT for digital tools and faster online quotes.

Business Insurance in Nevada: FAQ

Small business owners in Nevada often have questions about choosing the right business insurance. We answer the most common concerns below:

What insurance do I need for my small business in Nevada?

Nevada requires workers' compensation from your first employee and 25/50/20 commercial auto liability for work vehicles. Beyond legal minimums, you'll need general liability since Reno casinos and Las Vegas landlords won't sign contracts or leases without certificates. Compare options from ERGO NEXT, The Hartford or Simply Business to match your industry risks and budget.

How much does small business insurance cost per month in Nevada, and what factors affect the price most?

Your employee count, claims history and industry risk level affect rates most, but these are the monthly and annual averages by coverage type in Nevada:

- General liability: $117 monthly or $1,405 annually

- Workers' compensation: $84 monthly or $1,005 annually

- Professional liability (E&O): $88 monthly or $1,061 annually

- Business owner's policy (BOP): $167 monthly or $2,000 annually

Which companies are the best for small business insurance in Nevada (not just the cheapest)?

ERGO NEXT and The Hartford both earned 4.63 scores in MoneyGeek's Nevada analysis. ERGO NEXT provides same-day policies and instant certificates through mobile app, which is helpful when clients demand proof fast. The Hartford ranks first for claims satisfaction with 4.5 stars from 18,000+ reviews and offers Nevada's lowest rates. Choose based on your priorities.

Do I need workers' comp in Nevada if I only have 1 employee or I use 1099s?

Yes, Nevada requires workers' compensation from your first employee, even part-time or seasonal workers. True independent contractors (1099s) don't require coverage, but construction principal contractors remain liable for all job site workers. Misclassifying employees as 1099s triggers penalties up to three times owed premiums. Verify worker status with your insurance agent before hiring.

My client or landlord wants a COI. What limits do I need, and how fast can I get it?

Most Nevada contracts require $1 million general liability per occurrence with $2 million aggregate. Reno casinos and Las Vegas commercial properties often demand $2 million per occurrence. ERGO NEXT's mobile app provides instant certificates with unlimited additional insureds at no extra cost. The Hartford and Simply Business issue certificates within 24 hours.

About Mark Fitzpatrick

Mark Fitzpatrick, a Licensed Property and Casualty Insurance Producer, is MoneyGeek's resident Personal Finance Expert. He has analyzed the insurance market for over five years, conducting original research for insurance shoppers. His insights have been featured in CNBC, NBC News and Mashable.

Fitzpatrick holds a master’s degree in economics and international relations from Johns Hopkins University and a bachelor’s degree from Boston College. He's also a five-time Jeopardy champion!

He writes about economics and insurance, breaking down complex topics so people know what they're buying.

sources

- Nevada Consumer's Guide to Auto Insurance Rates. "2024 Auto Guide." Accessed March 24, 2026.

- Nevada Division of Industrial Relations. "Employer Coverage Requirements." Accessed March 24, 2026.

- Nevada Division of Insurance. "Nevada Division of Insurance Holding Town Hall Meeting on the Impact of Wildfire Threat on Insurance." Accessed March 24, 2026.

- Nevada Division of Insurance. "Nevada Division of Insurance Announces Consumer Home Insurance Tool." Accessed March 24, 2026.

- Nevada Revised Statutes. "Chapter 616A - Workers' Compensation." Accessed March 24, 2026.

- University of Nevada, Reno. "NSBDC Small Business Challenges Survey 2025." Accessed March 24, 2026.

- University of Nevada, Reno. "SBDC Small Business Survey Results 2023." Accessed March 24, 2026.