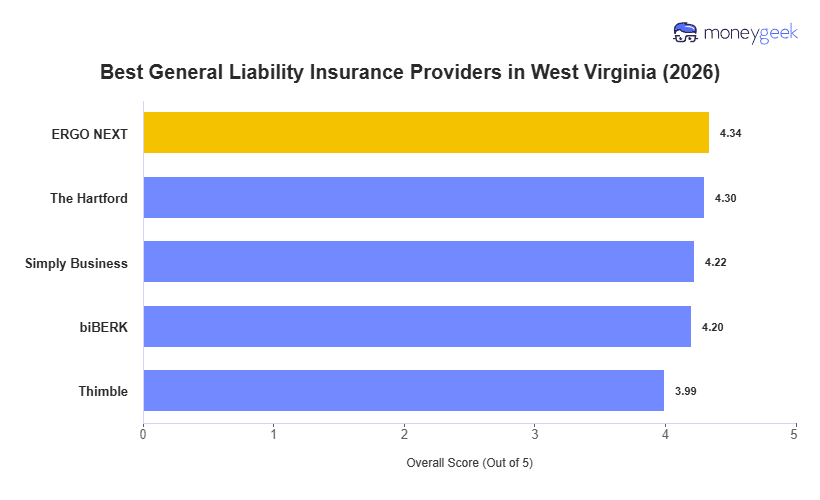

We evaluated 10 major general liability insurers across 408 business types at $1 million per occurrence/$2 million aggregate limits to identify the best and cheapest options for West Virginia small businesses. The five providers below ranked highest in the state, though the right match will vary by business:

- ERGO NEXT: Best Overall, Best for Hands-On Service Businesses

- The Hartford: Best Cheap General Liability Insurance

- Simply Business: Best Carrier Comparison Platform

- biBerk: Best for Leisure and Service Businesses

- Thimble: Best for Flexible, On-Demand Coverage

Rates and rankings for each provider are in the table below. A whitewater rafting outfitter near Fayetteville and a rural electrical contractor serving Mercer County both carry general liability coverage, but the right provider and rate for each will look different depending on the work and the risk.