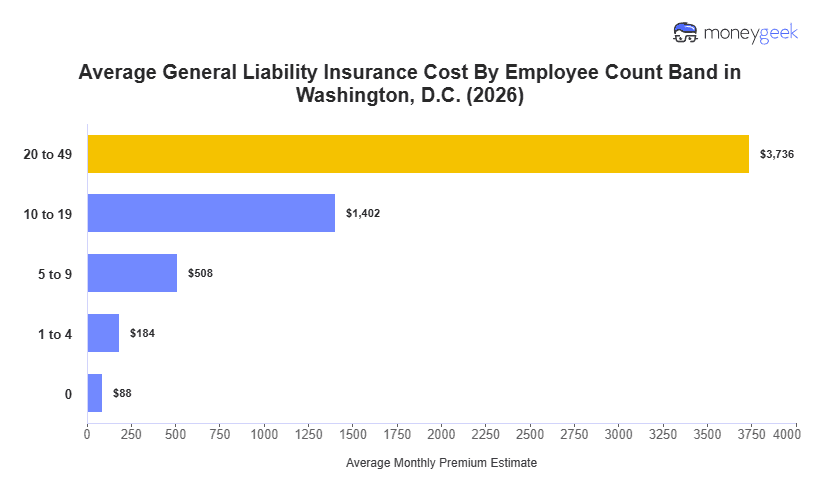

The average cost of general liability insurance for Washington, D.C. businesses with one to four employees runs $184 per month ($2,206 per year) at $1 million per occurrence/$2 million aggregate limits, 50% above the national average of $123 per month. D.C. ranks 50th for affordability, second only to California, making it one of the most expensive markets in the country.

The entire Mid-Atlantic and Northeast region sits above the national average, pointing to structural cost pressures rather than a D.C.-specific pricing anomaly. Dense urban markets carry higher liability exposure through greater foot traffic, concentrated contracted work and elevated litigation costs. D.C. leads the region, New York follows at $180 and Pennsylvania comes in closest to the national average at $129, a $55 spread that reflects how much market conditions vary even within the same region.

The $184 figure is a state average, not a rate or a prediction. The more useful question isn't how close your quote lands to that number, it's what's driving your cost to where it lands. To get a cost estimate based on your business profile, use the D.C. general liability insurance cost calculator below.