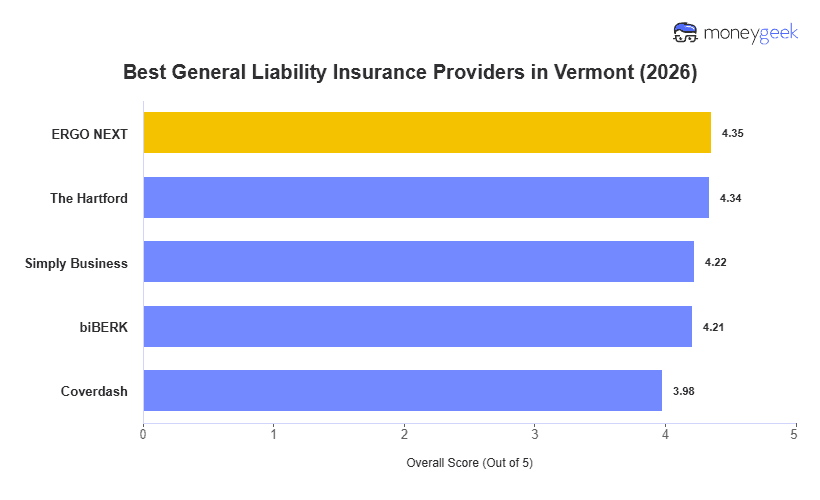

Vermont small businesses vary widely in risk and budget, and the right general liability provider for one won't always suit another. After scoring 10 major insurers across 408 business types to determine the best and cheapest options using $1 million/$2 million aggregate limits, these five consistently ranked at the top:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best for Professional And Institutional Businesses

- Simply Business: Best for Comparing Carriers

- biBerk: Best for Customer-Facing Businesses

- Thimble: Best for Freelancers and Seasonal Businesses

The table below lays out rates and rankings for each insurer so you can see how they compare. Your right fit will look different depending on your business. A contractor in Chittenden County and a farm-to-table restaurant in the Northeast Kingdom won't weigh the same factors.