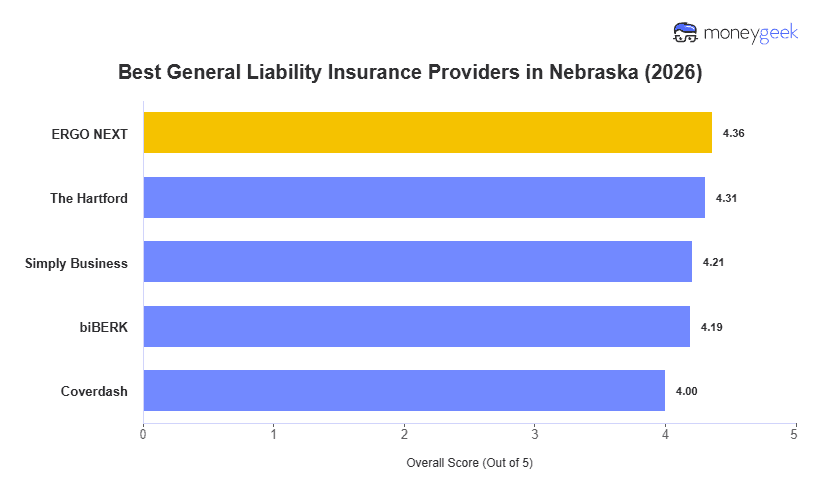

The right general liability coverage depends on your business type, risk level and budget. We evaluated 10 major insurers across 408 business types in Nebraska to identify the best and most affordable options. These five providers offer competitive rates and solid coverage for small businesses across the state.

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best for Professional and Office-Based Industries

- Simply Business: Best for Comparison Shopping

- biBerk: Best for Active Service Industries

- Coverdash: Best for Food and Beverage Businesses

Use the table below to compare rates and rankings side by side. A feedlot operator near Kearney and a boutique owner in Omaha's Dundee neighborhood have different liability exposures, so your best match depends on the risks your business actually carries.