Missouri small businesses have different risk profiles, budgets and coverage priorities. We analyzed 10 leading general liability insurers across 25 industries to find the best and cheapest performers, evaluated at standard $1 million/$2 million policy limits.

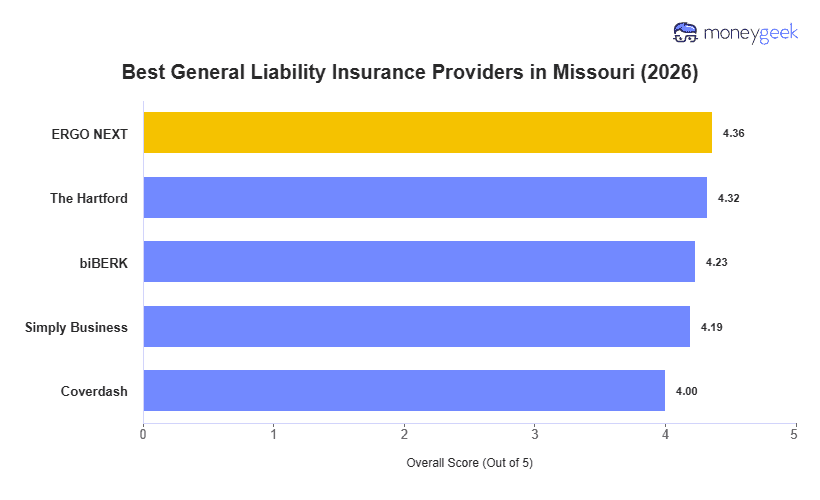

- ERGO NEXT: Best Overall, Best for Hands-On Service Businesses

- The Hartford: Best for Professional and Institutional Businesses

- biBerk: Best for Fitness, Recreation and Property Services

- Simply Business: Best for Comparing Carrier Options

- Coverdash: Best for Startups Needing Bundled Coverage

The table below breaks down rates and rankings for each provider. Whether you're running a barbecue food truck in Kansas City, a hair salon in Springfield, or a home repair business serving the Lake of the Ozarks area, you'll see how costs and coverage stack up for your situation.