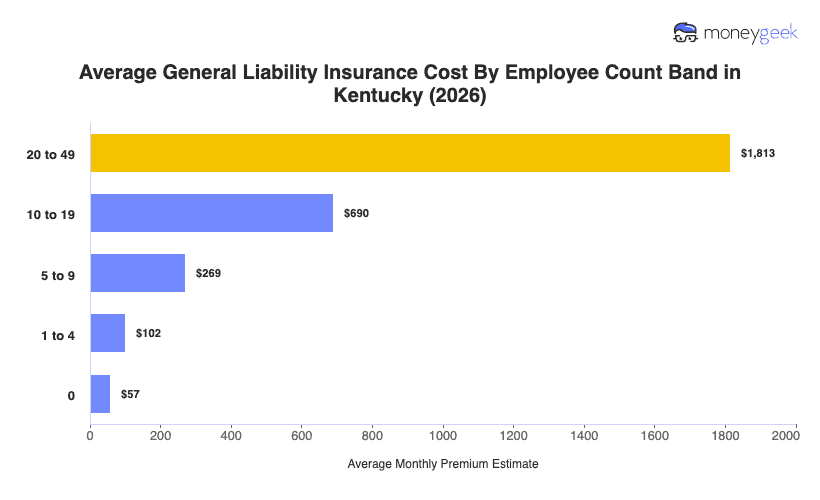

General liability insurance costs in Kentucky average $102 monthly ($1,222 annually) for businesses with one to four employees carrying limits of $1 million per occurrence/$2 million aggregate. This figure falls 17% below the national average, ranking Kentucky 13th for affordability nationally.

Kentucky lands near the middle of the broader South. Mississippi and Alabama average less at $89 and $100 monthly, while Tennessee, which also shares a border with Kentucky, sits higher at $112 monthly, along with other bordering states Indiana and Ohio. That spread reflects Kentucky's moderate regulatory and litigation environment, not a market under structural cost pressure.

The state average considers a wide array of general industries and shouldn't be treated as a rate prediction. More than how your quote compares to Kentucky's average, the more useful lens is understanding which factors explain where your premium lands. A more personalized cost estimate is available through the Kentucky general liability insurance cost calculator below.