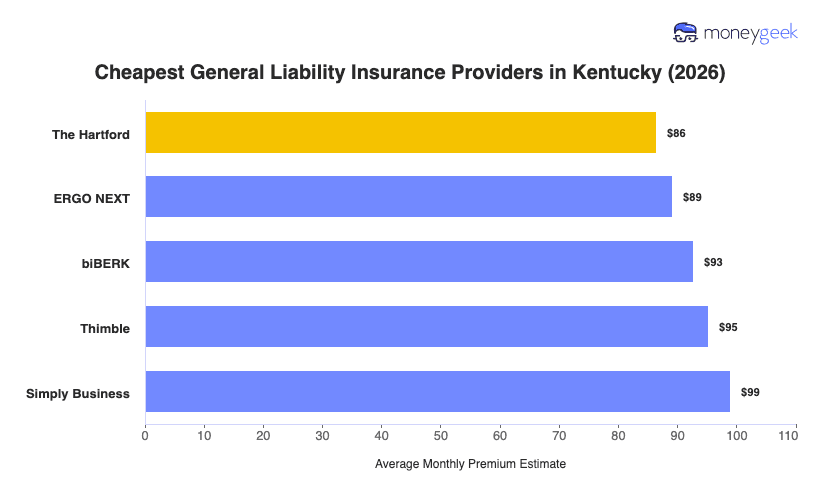

We analyzed 10 major providers across 408 business types at $1 million per occurrence/$2 million aggregate limits to find who prices lowest for Kentucky small businesses. While the that insurer comes out cheapest depends largely on what your business does, these five offer the most affordable general liability coverage for the state:

- The Hartford: Lowest rates for healthcare practices and professional and financial services (Allergist, Chiropractic Office, HR Consultant, Accounting Firm)

- ERGO NEXT: Most affordable for construction and skilled trades and beauty and personal care businesses (Electrical Contractor, HVAC Contractor, Hair Salon, Nail Salon)

- biBerk: Cheapest for cleaning and maintenance services and fitness and recreation businesses (House Cleaning Service, Janitorial Services, Gym/Fitness Center, Personal Training)

- Simply Business: Most affordable for retail storefronts and tech and software companies (Clothing Store, Hardware Store, Software Development, Managed Service Provider)

>> [Click each provider to learn more]

These groupings are a starting point, not a final answer: your actual rate shifts based on your revenue, payroll, employee count and claims history. Whether you're operating an equestrian boarding facility in the Bluegrass Region, a distillery tasting room along the Bourbon Trail or a home services business bracing for the state's harsh winter ice storms, compare quotes before locking anything in.