The average cost of general liability insurance for Kansas small businesses is $102 per month or $1,222 per year, 17% below the national average. Kansas ranks 12th nationally for affordability, putting it among the more affordable states in the country.

Kansas sits near the middle of both its adjacent states and the broader Midwest region. Oklahoma and Missouri, which border Kansas and share its regional market, have monthly premiums landing within $3, suggesting similar exposure profiles: moderate claim frequency, lower population density and a business mix that leans toward lower-risk operations. Colorado, which shares a border with Kansas but sits outside the Midwest region, averages $146, likely reflecting higher construction activity and greater urban exposure. Within the region, the Dakotas and Iowa run meaningfully cheaper, while Minnesota is the only Midwest state that exceeds the national average.

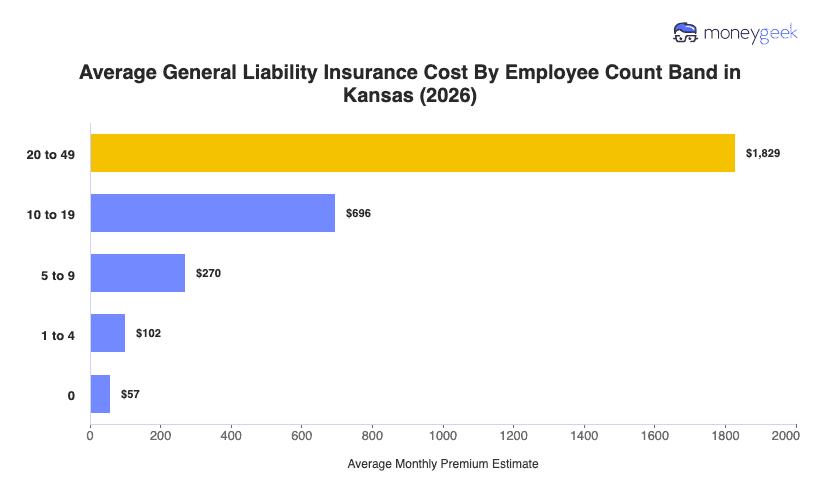

Kansas' state average cuts across business types and isn't a rate prediction. The more useful question is what's driving your cost, not just how close your quote is to the benchmark. For an estimate closer to your actual profile, the Kansas general liability insurance cost calculator below accounts for your specific business details.