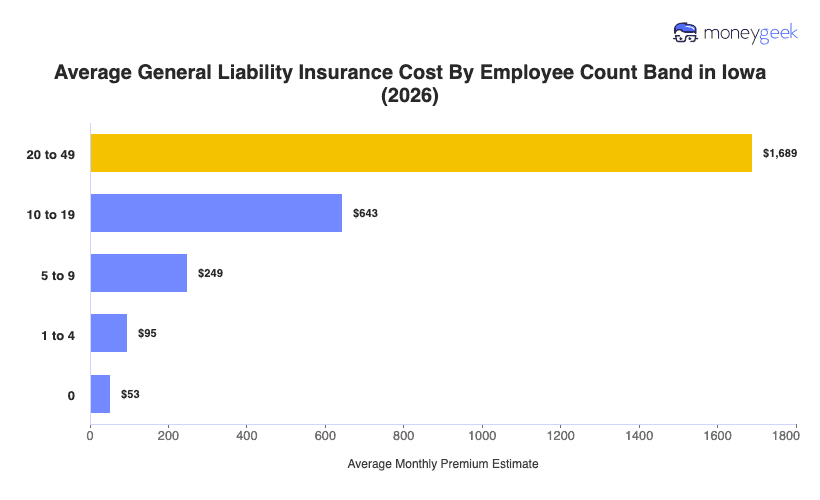

The cost of general liability insurance for small Iowa businesses with one to four employees is $95 monthly ($1,135 annually) for coverage limits of $1 million per occurrence/$2 million aggregate limits. That makes Iowa the fourth most affordable state for general liability coverage, as its average monthly rate falls 23% below the national figure of $123.

Most of Iowa's neighboring states are more expensive, with Nebraska being the closest at $105 monthly. Minnesota and Illinois are 36% and 48% higher. Beyond border states, Midwest pricing compresses into a narrower range: North Dakota nearly matches Iowa at $96 monthly, while Kansas and Missouri both hover near $105. Most regional states fall within a narrow $10 band, with Iowa and North Dakota forming the low end.

This state average serves as a starting reference. The useful comparison isn't "Am I near $95?" but "Which drivers explain my distance from it?" Industry claim frequency, operational risk controls and prior loss experience all contribute to where your quote lands, regardless of the limits you select. To get a cost estimate based on your business profile, use the Iowa general liability insurance cost calculator below.