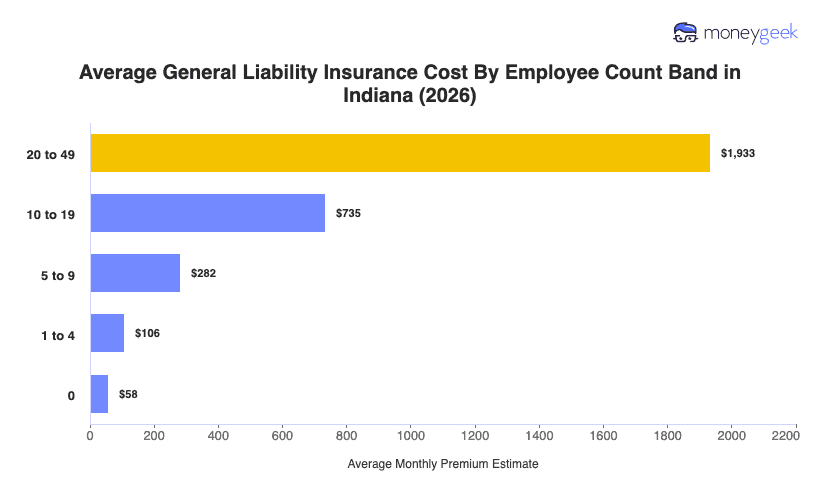

The average cost of general liability insurance in Indiana averages $106 monthly ($1,272 annually) for businesses with one to four employees and coverage limits of $1 million per occurrence/$2 million aggregate. Indiana is the 19th most affordable state, with its monthly cost falling 14% below the national benchmark.

Indiana's premiums are consistently lower than neighboring states across the Midwest. Wisconsin, Ohio and Michigan come closest to its monthly average, all with rates less than 10% higher. Illinois, at $141 monthly, is 33% more expensive, driven by elevated claim costs and a more aggressive commercial liability environment.

The statewide average provides a reference point for comparison rather than a guaranteed price. Your final premium shifts based on industry-specific claim exposure, operational risk factors and historical loss experience, even when businesses select identical coverage limits. For an estimate closer to your actual profile, the Indiana general liability insurance cost calculator below accounts for your specific business details.