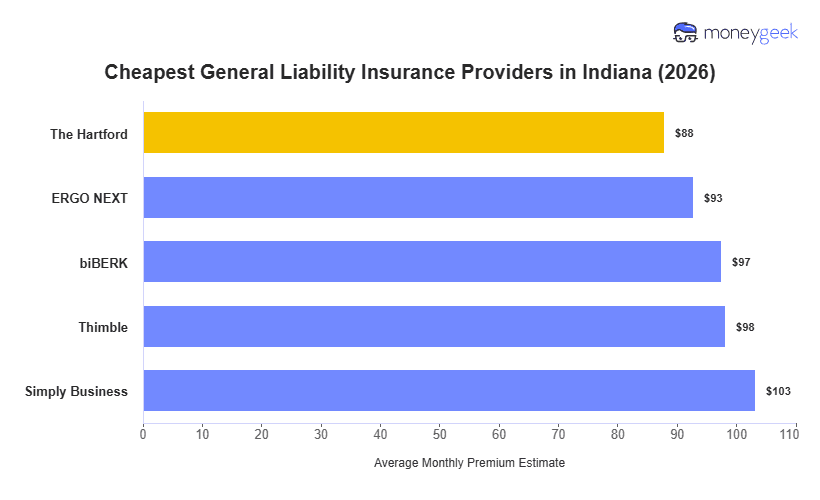

Based on our analysis of 408 industries in Indiana, these are the three cheapest general liability insurance providers in the state:

- The Hartford: Cheapest for professional services and creative businesses (management, IT, photography, videography)

- ERGO NEXT: Most affordable for trades and customer-facing operations (roofing, painting, barber shops, tattoo shops)

- biBERK: Cheapest for healthcare and fitness businesses (chiropractors, physical therapy, yoga studios, CrossFit gyms)

>> [Click Each Provider To Learn More]

Rates vary based on your specific industry, revenue, employee count and claims history in Indiana, so use these providers as a starting point for comparing quotes tailored to your business.