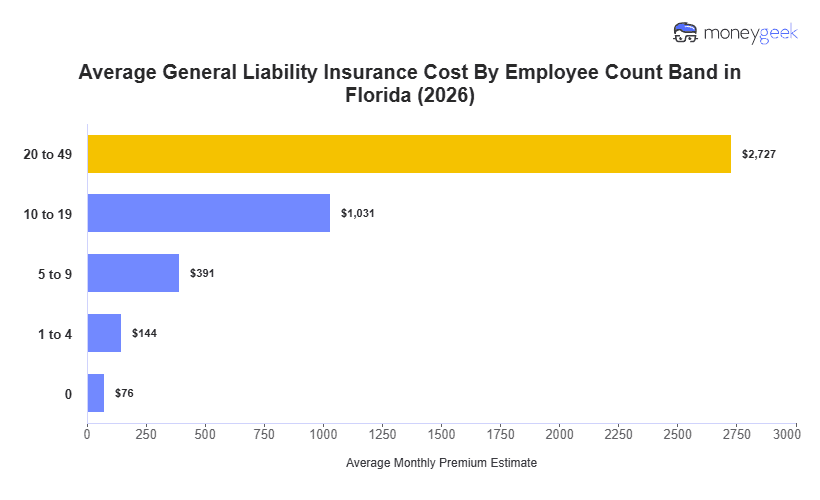

Small businesses in Florida pay $144 monthly ($1,732 annually) for general liability coverage, about 17% above the national average. Despite this below-average cost, the state ranks 40th nationally for affordability.

Within the Southeast, Florida sits in the higher-cost tier. Its two neighboring states are both cheaper: Alabama averages $100 monthly (ranking 10th nationally) and Georgia comes in at $121 (27th). Across the broader region, only Maryland exceeds Florida's general liability costs at $155, while other states like North Carolina and Delaware also price below it. The state's elevated costs likely stem from higher litigation rates and slip-and-fall claim frequency in tourist-heavy and hospitality sectors that drive up liability premiums statewide.

Florida's average benchmark serves as an initial reference point, though actual costs vary with industry risk profile and claims environment. The state's position above most regional peers indicates that location accounts for measurable cost differences within the Southeast, a factor to weigh when comparing quotes or evaluating whether operations in a neighboring state might reduce premiums. For an estimate closer to your actual profile, the Florida general liability insurance cost calculator below accounts for your specific business details.