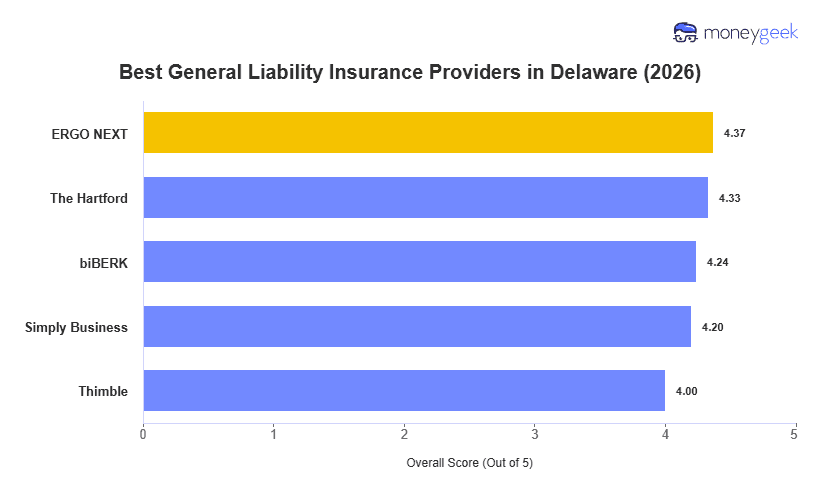

Choose the right general liability coverage by knowing which insurers offer consistent value in your state. We evaluated 10 major providers across 25 general industries in Delaware, comparing rates, service quality and policy flexibility. The five below represent the best and cheapest options for Delaware small businesses:

- ERGO NEXT: Best Overall, Best for Hands-On and Service Industries

- The Hartford: Best Cheap General Liability Insurance

- biBerk: Best for Solo Operators

- Simply Business: Best for Food and Wholesale Businesses

- Thimble: Best for Short-Term and Project-Based Coverage

Your ideal general liability match depends on your exposure and budget, whether you run a corporate services firm in Wilmington or a retail shop near Rehoboth Beach. This table breaks down monthly rates and overall rankings so you can compare options side by side.