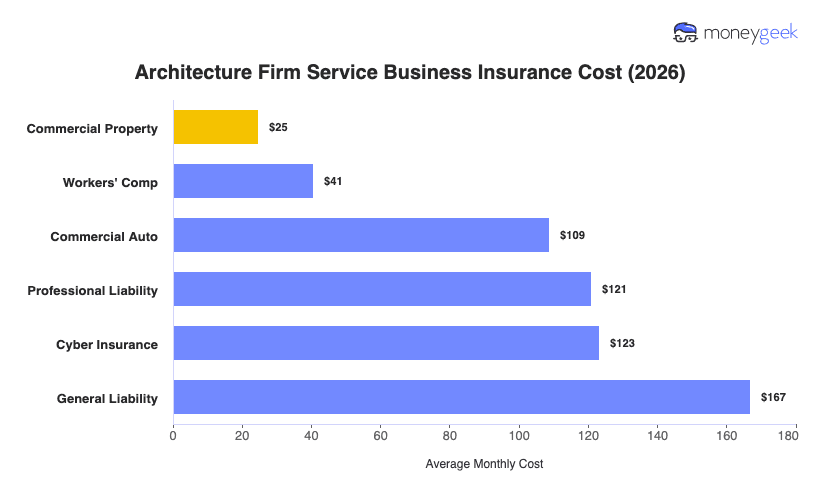

Contractor business insurance costs for architecture firms average around $98 a month or $1,171 per year across six common coverage types. We determined these figures by analyzing quotes from architecture firms with one to four employees across 50 states and Washington, D.C., carrying standard policy limits of $1 million per occurrence and $2 million aggregate.

Individual coverage costs range from $25 to $167 a month, with commercial property having the lowest rates on average because your studio workstations and office contents represent a bounded, fixed-location asset base that insurers price accordingly. General liability costs the most and reflects your construction site exposure and the near-universal requirement that clients, landlords and project contracts carry it.

The table below shows average monthly costs by coverage type, but treat these figures as benchmarks for your firm's profile, not quotes.