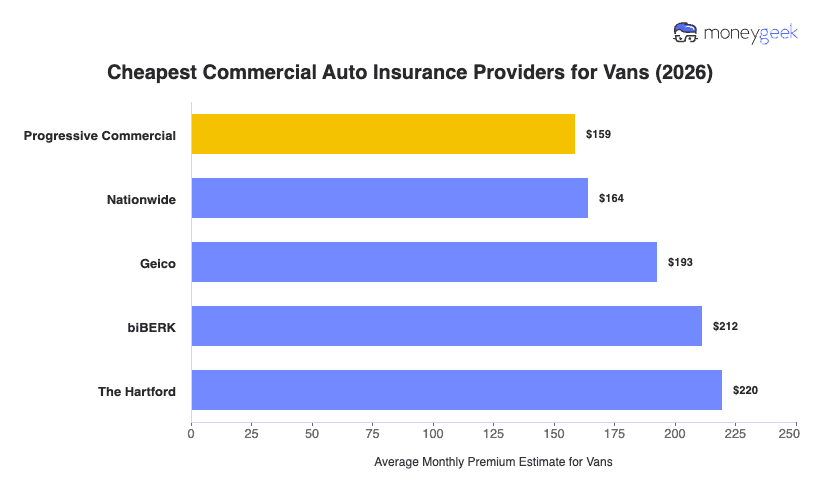

These are the cheapest commercial auto insurers for vans and how they perform for various industry categories:

- Progressive Commercial: Averages $159 per month for commercial van insurance, 16% below the provider average. It ranks cheapest across 15 of the 22 industries, with its strongest savings showing up for childcare businesses ($123 per month), education businesses ($128 per month), pet care services and real estate operations.

- Nationwide: Averages $164 per month, 13% below the provider average. It prices lowest for consulting services ($110 per month), agriculture and natural resources ($122 per month), recreation and sports, and other professional services.

- GEICO: Averages $193 per month, about 2% above the provider average. It doesn't rank first for affordability in any industry, but it prices close to or below average for tech, fitness and arts businesses.

- biBerk: Averages $212 per month, 12% above the provider average. It is the cheapest provider for tech and IT businesses ($108 per month), fitness businesses ($110 per month) and arts, media and entertainment operations ($139 per month).

- The Hartford: Averages $220 per month, 16% above the provider average. Businesses that prioritize claims service may find The Hartford worth comparing, but it won't be the cheapest option for most van operators.

The rates above are based on a sample profile. Your actual commercial van insurance costs will shift based on your vehicle use classification, driver records, annual mileage and coverage selections. Though these rankings won't match every business exactly, you can use them as a starting point and compare quotes with identical coverage terms to find your real cheapest option.