North Carolina's commercial auto rankings come down to three things: what businesses in the state actually pay for coverage, what happens when they need support and whether the policy holds up when a claim is filed. Each provider was scored across affordability (50%), customer experience (30%) and coverage options (20%), weighted that way because price is where most North Carolina businesses start the search, but it's rarely where the decision should end. For the full breakdown, see the methodology.

Best Commercial Auto Insurance in North Carolina

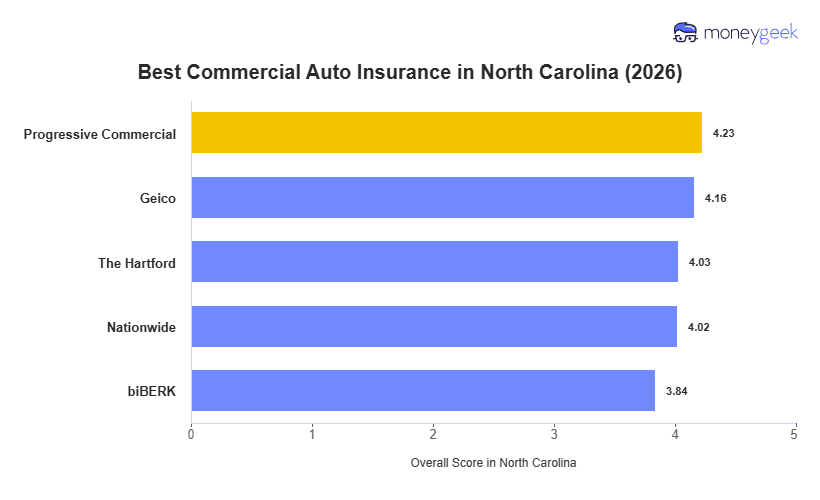

Progressive Commercial, GEICO and The Hartford are the strongest commercial auto insurance options in North Carolina, based on affordability, customer experience and coverage options.

Progressive Commercial ranks first overall in North Carolina, but the right fit for your business depends on your vehicle type, industry and specific coverage needs.

Get matched to your best commercial auto insurer and get quotes in minutes using our tool below.

Select state

Updated: May 22, 2026

Advertising & Editorial Disclosure

How We Built These Best Small Business Insurer Rankings

Top Picks: Best Commercial Auto Insurance Companies in North Carolina

No single insurer is the right commercial auto option for every North Carolina business, and the data behind this list makes that clear. Progressive Commercial leads overall, but the right carrier comes down to three things specific to the operation: what vehicles the business operates, what a serious claim would cost the business and how much support it needs when something goes wrong. Those factors play out differently across North Carolina's business landscape, which is why the right answer for a Charlotte-based construction contractor running a fleet of work vans looks nothing like the right answer for a solo agricultural operator in the eastern part of the state.

Each provider below earned its spot for a specific reason, and that reason matters more than the overall ranking when a business has a particular vehicle profile, risk level or set of priorities. The best commercial auto insurance for one operation can be the wrong call for another:

- Progressive Commercial: Best Overall, Best for Fleet Operations

- GEICO: Best for Low-Risk Business Areas

- The Hartford: Best for Coverage Depth

- Nationwide: Best for Agricultural and Specialty Fleets

- biBERK: Best for Simple Coverage Needs

The table below shows how all five ranked in this analysis for a side-by-side comparison.

| Progressive Commercial | 4.23 | 2 | 1 | 4 |

| Geico | 4.16 | 1 | 2 | 3 |

| The Hartford | 4.03 | 5 | 2 | 1 |

| Nationwide | 4.02 | 3 | 5 | 2 |

| biBERK | 3.84 | 4 | 4 | 5 |

The summaries below lay out exactly who each provider fits best and who should look elsewhere, because overall rankings mean nothing if a provider doesn't match the specific vehicle type, industry or operational need.

Progressive

Best Overall, Best for Fleet Operations

Progressive Commercial holds the largest share of the commercial auto market in the country, and in North Carolina that scale translates into real pricing advantages across vehicle types that most carriers can't match consistently. It prices below the state average on taxis, limousines, food trucks and vans, and its customer experience score pulls away from the other four providers by a meaningful margin. That combination of competitive rates and post-purchase support makes it the most well-rounded option on this list for businesses running multiple vehicles or operating in higher-exposure categories. The one area where it gives ground is coverage depth: its coverage score ranks fourth among the five, so if your operation needs broad endorsement options or specialized policy structures, The Hartford is worth a direct comparison. For most North Carolina fleet operators, though, Progressive Commercial is the right place to start.

Learn More: Progressive Business Insurance Review

GEICO

Best for Low-Risk Business Areas

Part of Berkshire Hathaway's insurance group, GEICO has spent over 70 years building its reputation on competitive pricing and straightforward digital access, and that combination shows up clearly in its North Carolina commercial auto numbers. It ranks second overall and first on affordability across the five providers, posting the strongest rates on farm tractors, sedans, SUVs and pickup trucks. That vehicle mix tells you a lot about who GEICO works best for: businesses running standard light commercial vehicles in lower-exposure categories, where its pricing advantage is sharpest and its digital-first model fits the operation. Where it gives ground is customer experience, which ranks third among the five providers, and its coverage score sits in the middle of the field. North Carolina businesses in professional services, consulting, real estate and similar low-mileage, office-based operations will find GEICO the most cost-effective option on this list.

The Hartford

Best for Coverage Depth

Founded in 1810, The Hartford brings more than two centuries of commercial insurance experience to North Carolina's market, and that depth shows up most clearly in its coverage score, which leads all five providers in this analysis. It ranks first on coverage options, offering the broadest policy structures, the widest endorsement availability and the most flexibility across coverage tiers of any carrier on this list. The tradeoff is price: The Hartford ranks last on affordability overall, coming in above the North Carolina average on every vehicle type. That gap is most pronounced on farm tractors and pickup trucks, where other providers price considerably lower. But for North Carolina businesses where coverage quality and claims reliability matter more than finding the lowest rate, particularly operations in construction, healthcare or transportation where a coverage gap at claim time carries real financial consequences, The Hartford is the strongest option on this list for policy depth.

Learn More: The Hartford Business Insurance Review

Nationwide

Best for Agricultural and Specialty Fleets

Nationwide was founded in 1926 by the Ohio Farm Bureau Federation specifically to serve farmers who couldn't get fair coverage from traditional insurers, and that agricultural DNA is still visible in its commercial auto product nearly a century later. It ranks fourth overall in North Carolina but tells a more nuanced story than that position suggests: its coverage score ranks second among the five providers, and its agricultural and specialty fleet infrastructure is deeper than anything else on this list. The affordability picture is mixed. Nationwide prices competitively on limousines and vans but comes in above the North Carolina average on farm tractors and pickup trucks, which is a meaningful limitation given how central those vehicle types are to the state's agricultural and construction sectors. Its customer experience score ranks last among the five providers, which is the most important caveat for any North Carolina business owner who values post-purchase support. For operations in agriculture, food processing or specialty fleet categories where coverage structure matters more than rate or service scores, Nationwide is worth a serious look.

Learn More: Nationwide Commercial Auto Insurance Review

biBerk

Best for Simple Coverage Needs

biBERK is Berkshire Hathaway's direct-to-consumer small business insurance brand, built around one idea: get covered online without a broker, an agent or a waiting room. Founded in 2015, it's the newest provider on this list and the most narrowly focused. In North Carolina it ranks fifth overall, and the data reflects its positioning accurately. Its affordability score is competitive on sedans and SUVs, two vehicle types common in low-exposure, office-based operations, but it prices above the state average on every high-exposure vehicle category including taxis, limousines and food trucks, sometimes by a wide margin. Its coverage score ranks last among the five providers, which is a real limitation for any North Carolina business with complex fleet needs or specialized risk. What biBERK does well is exactly what it's designed to do: a straightforward digital purchase process, Berkshire Hathaway's financial backing and A++ AM Best ratings, and a policy structure that works cleanly for small businesses that know what they need and don't require much hand-holding after purchase. For a North Carolina sole proprietor or micro-business running one or two standard vehicles in a low-risk industry, biBERK is a practical and financially sound option.

Learn More: biBerk Business Insurance Review

Best North Carolina Commercial Auto Insurance by Vehicle Type

Progressive Commercial ranks first across seven of eight vehicle types in North Carolina, with its strongest rate advantages in high-exposure categories like taxis and limousines, where it runs about 31% below the state average. But for North Carolina businesses running farm tractors as their primary commercial vehicle, GEICO offers better value and leads on that vehicle type specifically.

| Farm Tractor | Geico | 1 | 2 | 3 |

| Food Truck | Progressive Commercial | 1 | 1 | 4 |

| Limousine | Progressive Commercial | 1 | 1 | 4 |

| Pickup Truck | Progressive Commercial | 2 | 1 | 4 |

| SUV | Progressive Commercial | 2 | 1 | 4 |

| Sedan | Progressive Commercial | 3 | 1 | 4 |

| Taxi | Progressive Commercial | 1 | 1 | 4 |

| Van | Progressive Commercial | 1 | 1 | 4 |

Vehicle type affects pricing more than most North Carolina businesses expect. Here's how the top North Carolina providers compare across vehicle types in this analysis:

Best Commercial Auto Insurance in North Carolina by Industry

GEICO ranks first in 16 of 25 industries in North Carolina, posting its strongest overall scores across consulting, financial services, tech/IT, marketing and communications, and fitness services, categories where low-mileage light vehicles are the norm and its pricing advantage is sharpest. Progressive Commercial leads in the remaining nine industries, including food and beverage, construction and contracting, and transportation and logistics, where its customer experience score tops all five providers and its rates stay competitive on the heavier vehicle types those industries rely on.

| Agriculture & Natural Resources | Geico | 1 | 2 | 3 |

| Arts, Media & Entertainment | Progressive Commercial | 4 | 1 | 4 |

| Beauty, Body & Wellness Services | Geico | 1 | 2 | 3 |

| Childcare Services | Progressive Commercial | 1 | 1 | 4 |

| Cleaning Services | Progressive Commercial | 1 | 1 | 4 |

| Construction & Contracting | Progressive Commercial | 2 | 1 | 4 |

| Consulting Services | Geico | 1 | 2 | 3 |

| Education | Progressive Commercial | 2 | 1 | 4 |

| Financial Services | Geico | 1 | 2 | 3 |

| Fitness Services | Geico | 1 | 2 | 3 |

| Food & Beverage | Progressive Commercial | 1 | 1 | 4 |

| Healthcare & Medical | Progressive Commercial | 2 | 1 | 4 |

| Hospitality, Travel & Tourism | Progressive Commercial | 1 | 1 | 4 |

| Manufacturing | Progressive Commercial | 1 | 1 | 4 |

| Marketing & Communications | Geico | 1 | 2 | 3 |

| Nonprofit & Associations | Progressive Commercial | 1 | 1 | 4 |

| Other Professional Services | Progressive Commercial | 1 | 1 | 4 |

| Pet Care Services | Progressive Commercial | 2 | 1 | 4 |

| Real Estate & Property Services | Progressive Commercial | 2 | 1 | 4 |

| Recreation & Sports | Progressive Commercial | 2 | 1 | 4 |

| Repair & Maintenance | Progressive Commercial | 1 | 1 | 4 |

| Retail & Product Rental | Progressive Commercial | 1 | 1 | 4 |

| Tech/IT | Geico | 1 | 2 | 3 |

| Transportation & Logistics | Progressive Commercial | 1 | 1 | 4 |

| Wholesale & Distribution | Progressive Commercial | 1 | 1 | 4 |

Dedicated resources are available to help North Carolina businesses find the best commercial auto insurance for their specific industry.

What Determines the Best Commercial Auto Insurance in North Carolina for You

The best commercial auto insurance in North Carolina isn't defined by a single factor. The right provider balances affordability, coverage depth and customer experience across the vehicle types and industries most common in the state.

Three areas matter most when evaluating which insurer fits your business.

Affordability Across Your Vehicle Type and Industry

Affordability Across Your Vehicle Type and IndustryNorth Carolina commercial auto pricing varies more by vehicle type and industry than most businesses expect, and the gaps are wide enough to matter. Taxi and limousine operators, for example, see rate differences of 30% or more between the most and least affordable providers in this analysis. Pickup trucks and sedans, common in construction and professional services across the state, also show meaningful variation. The industry you operate in compounds the effect: a food and beverage business and a consulting firm running identical vehicles will pay very different rates. Starting with your actual vehicle type and industry, rather than a general rate comparison, gets you to a more accurate picture faster.

Coverage That Matches Your Fleet's Risks

Coverage That Matches Your Fleet's RisksNorth Carolina requires minimum liability coverage of 50/100/50, meaning $50,000 per person for bodily injury, $100,000 per accident and $50,000 for property damage. Uninsured and underinsured motorist coverage at the same limits is also mandatory on all new and renewed policies as of July 1, 2025. Those minimums are the floor, not a recommendation.

Coverage decisions that go beyond the minimums include:

- Liability limits above 50/100/50, which matter most for North Carolina businesses in construction, transportation and healthcare where a serious claim can exceed minimum thresholds quickly

- Breadth of vehicles covered, particularly for operations mixing owned, leased and employee-used vehicles common in real estate, healthcare and field services

- Hired and non-owned auto coverage for industries where employees regularly use personal vehicles for business purposes

- Cargo and equipment protection for North Carolina's agriculture, food processing and manufacturing operations

- Standard versus endorsement-only coverage structures, which affect what's actually included without an additional premium

- Deductible flexibility and coverage for fleet growth, both relevant for businesses adding vehicles mid-policy

For-hire property carriers operating vehicles with a gross vehicle weight rating above 10,000 pounds must carry a minimum of $750,000 in liability coverage under North Carolina and federal FMCSA requirements. Interstate operations trigger additional filing requirements including a USDOT number, MC number and BMC-91 filing. Passenger carriers charging fares must carry between $1.5 million and $5 million in combined single limit coverage depending on seating capacity.

Customer Experience and Claims Support

Customer Experience and Claims SupportA commercial auto policy is only as useful as the carrier behind it when something goes wrong. For North Carolina businesses, that means evaluating how each provider handles claims: whether filing is available 24/7, how long resolution typically takes and what commercial policyholders consistently report about the process. NAIC complaint ratios offer one objective data point. Direct evaluation of each provider's policy management tools, digital access and agent availability rounds out the picture. The difference between a carrier that resolves a claim in days and one that takes weeks is a real operational cost for any business that depends on its vehicles.

How to Choose the Best Commercial Auto Insurance in NC

Choosing the right commercial auto insurance in North Carolina requires more than comparing premiums. These steps allow you to make the most informed decision for your business.

- 1Define Your Risk Profile

Start by documenting every vehicle your business operates in North Carolina, including owned, leased and employee-owned vehicles used for business purposes. Record primary use, annual mileage and the driving records of everyone behind the wheel. North Carolina businesses in construction, agriculture, food processing and transportation should pay particular attention to load type and mileage, since both directly affect pricing and eligibility across the five providers in this analysis.

- 2Determine Your Coverage Requirements

With your risk profile in hand, identify which coverage types your operations actually require beyond North Carolina's 50/100/50 minimum liability limits and mandatory UM/UIM coverage. For example:

- Businesses transporting goods in North Carolina need cargo coverage, which is particularly relevant for food processors, agricultural distributors and manufacturing operations across the state.

- Financed or leased vehicles require collision and comprehensive coverage.

- Operations relying on employee-owned vehicles need hired and non-owned auto coverage.

- For-hire property carriers operating vehicles with a GVWR above 10,000 pounds must carry a minimum of $750,000 in liability coverage under state and federal requirements.

- Passenger carriers charging fares must carry between $1.5 million and $5 million in combined single limit coverage depending on seating capacity.

Match coverage types to real operational needs in North Carolina rather than assumptions.

- 3Research Providers by Industry and Vehicle Type

Not every carrier prices every risk the same way in North Carolina. Some providers price high-exposure vehicles like taxis and limousines far more competitively than others, while carriers like GEICO offer stronger value for standard light commercial vehicles in lower-risk industries. Identify which carriers have demonstrated strength in your specific vehicle category and industry before comparing them on price.

- 4Evaluate Coverage Quality and Policy Terms

Comparing premiums tells you what a policy costs. Comparing policy terms tells you what you're actually buying. For each provider on your shortlist, check which coverages are standard versus endorsement-only, what liability limits are available above North Carolina's 50/100/50 minimum and what exclusions could affect a claim. Confirm how the policy handles mid-term fleet changes, since adding vehicles during a policy period creates temporary coverage gaps with some carriers.

- 5Get Quotes to Confirm

Request quotes only after narrowing your options through research. North Carolina commercial auto pricing varies meaningfully by vehicle type, industry and location within the state. A quote from a provider that doesn't specialize in your vehicle category or industry may not reflect what you'd actually pay. Use quotes to validate your shortlist, not to build it.

- 6Confirm North Carolina Filing Requirements

Verify whether your operation triggers additional filing requirements before purchasing a policy. North Carolina businesses operating vehicles with a GVWR above 10,000 pounds for interstate for-hire transport must obtain a USDOT number and MC number from the FMCSA, file a BMC-91 insurance filing and designate a process agent through a BOC-3 filing. Intrastate for-hire passenger carriers and hazmat operators face separate state-level requirements under North Carolina General Statutes. Confirming these requirements before purchase avoids coverage gaps and delays in getting your authority active.

Best Commercial Auto Insurance in North Carolina: Bottom Line

Three questions cut through most of the noise when comparing commercial auto insurance in North Carolina: What vehicles does your business operate? What industry are you in? And what would a serious claim actually cost your operation? Your answers to those three questions narrow the field faster than any rate comparison, because pricing and coverage depth vary more by vehicle type and industry than most North Carolina businesses expect. Start there before you look at a single quote.

From there, think about two things: whether the cheapest policy actually covers your operation's real exposure, and whether you want a fully digital self-service experience or a carrier with more hands-on agent support. Those two dimensions alone will point you toward different providers on this list. Once you have a shortlist based on fit, get two or three quotes to confirm whether the pricing holds for your specific fleet, location and coverage requirements in North Carolina.

Best Commercial Auto Insurance: Next Steps

For most North Carolina businesses, the right starting point is getting quotes from Progressive Commercial and GEICO. Progressive Commercial leads on customer experience and prices competitively across the widest range of vehicle types in the state, making it the strongest all-around option for fleet operators and higher-exposure categories. GEICO is the better starting point for office-based operations, professional service businesses and agricultural operators running standard light vehicles or farm tractors, where its affordability advantage is most pronounced. If your business operates in a regulated industry, runs high-exposure vehicles or needs deeper coverage structures, add The Hartford to your list.

Recommended: If You're Ready to Get Quotes Now

By this point you should know your fleet composition, your coverage requirements and which providers align with your industry and vehicle type in North Carolina. Request quotes from at least three providers and compare both price and policy terms before committing. If a quote comes back higher than expected, check your coverage selections and driver records first before moving on from a provider that otherwise fits your operation.

If You Want to Confirm Cost Before Deciding

North Carolina commercial auto pricing shifts more by vehicle type and industry than most published averages reflect. A food truck operator and a financial services firm running the same vehicle in the same city can see very different rates across the same five providers. Use the resources below to ground your cost expectations before reaching out to any carrier.

If You're Unsure What Coverage Your Fleet Needs

Start by mapping your actual exposure: what vehicles you operate, how they're used, what they carry and whether employees use personal vehicles for business in North Carolina. Each of those factors points to a specific coverage type, and missing one creates a real gap in financial protection.

If You Have Specialized Filing Requirements

North Carolina businesses operating vehicles with a GVWR above 10,000 pounds for interstate for-hire transport, running passenger carrier services that charge fares or hauling hazardous materials need to confirm their filing requirements before purchasing a policy. These operations must obtain a USDOT number, file a BMC-91 through their insurer and designate a process agent via BOC-3 before their authority becomes active. Passenger carriers charging fares face separate state-level requirements under NCAC Rule R2-36, with minimum coverage ranging from $1.5 million to $5 million depending on seating capacity. Getting these filings in order before you buy prevents delays and coverage gaps on day one.

How We Chose the Best North Carolina Commercial Auto Insurance Companies

Our goal was to identify which providers deliver the most consistent overall value across the three dimensions that matter most to business owners: what they pay, how well they're covered and how the carrier performs when they need support. Five providers made the cut for our North Carolina analysis: Progressive Commercial, GEICO, The Hartford, Nationwide and biBerk. We analyzed all five across all eight vehicle types and 25 general industry categories covering more than 400 specific industry areas.

Our Scoring Model

We scored each of the five providers across three weighted categories that combine into an overall score out of 5.

- Affordability (50% of overall score): We measured how competitively and consistently each provider prices commercial auto coverage across vehicle types, industries and states, benchmarked against national average rates.

- Customer Experience (30% of overall score): We evaluated how well each provider supports businesses across the full policy lifecycle — buying, policy management and claims handling.

- Coverage Options (20% of overall score): We assessed how well each provider addresses common commercial fleet risks and how much flexibility it allows across coverage types and endorsements.

Learn more about our methodology.

About Connor Bolton

Connor Bolton is Senior SEO and Content Manager at MoneyGeek, where he leads the business and pet insurance editorial teams. He sets the research framework, data standards and content structure for his team. All content goes through his accuracy review before publication. Connor also writes in-depth guides and has spent more than four years covering insurance products across personal, commercial and specialty lines.

The research infrastructure Connor built covers auto, home, renters, life, health, business and pet insurance across pricing analysis, carrier research, customer experience and coverage evaluation. It includes over 6 million data points for business insurance across 408 industry areas, all 50 states and 16 vehicle types. The pet insurance side covers over 5 million profiles across 18 major providers, 100+ breeds and ages up to 20 years. Connor’s insurance research and his team's work has been cited by the U.S. Chamber of Commerce, Allstate, Liberty Mutual, CBS News, Forbes and LegalZoom.

Connor also talks with underwriters and carrier liaisons at Ethos, The Hartford, ERGO NEXT, Nationwide and State Farm, and monitors business and pet owner communities on Reddit. Those sources shape how his team evaluates carriers, structures rate analysis and writes for human buyers rather than search engines.

For questions about MoneyGeek's business and pet insurance content, contact him at connor@moneygeek.com or on LinkedIn.