A $10 million jury verdict used to be a problem for Fortune 500 companies and major insurers. In 2024, it became a problem for the small businesses next door.

Small businesses with $10 million or less in revenue now carry 48% of U.S. commercial tort costs, even though they generate just 20% of commercial revenue, according to a 2023 Institute for Legal Reform analysis of Brattle Group data covering 2021. That works out to about $35 in tort costs for every $1,000 of revenue, versus less than $5 per $1,000 for the largest companies.

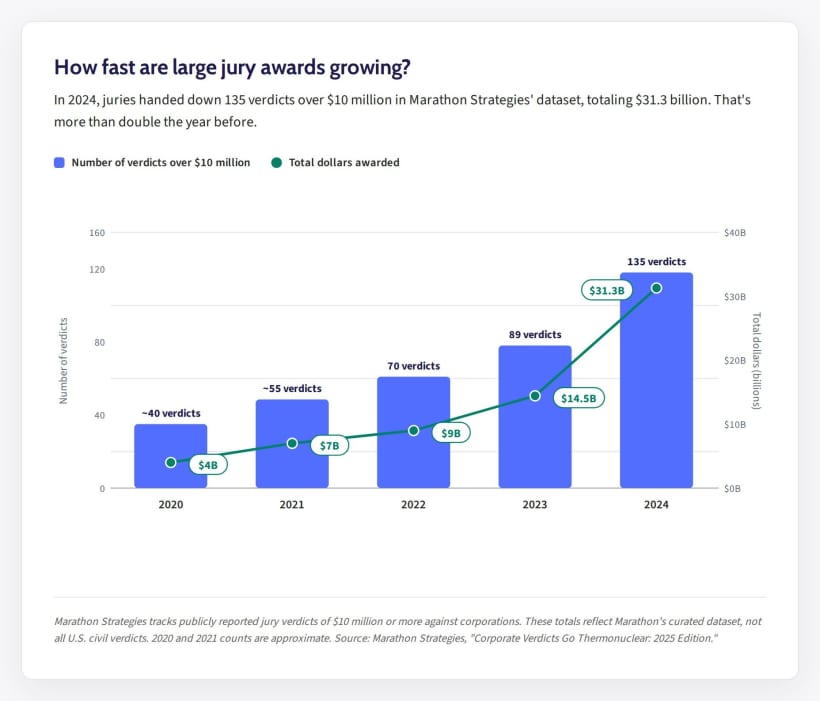

Nuclear verdicts, defined as jury awards of $10 million or more, hit a record $31.3 billion in 2024 according to Marathon Strategies, a 116% jump from the year before. A 2025 Swiss Re behavioral study found that in legal simulations, respondents awarded damages against small and midsize companies at nearly the same rate as against large corporations when injuries were serious. Yet most small business general liability policies cover just $1 million per occurrence. A single nuclear verdict could exceed that limit by $9 million or more before any umbrella coverage applies.