The average cost of general liability insurance in South Carolina is $96 monthly ($1,154 annually) for most businesses, 22% below the national average. This positions South Carolina as the sixth most affordable state nationally, with costs running $27 lower per month than the typical U.S. business pays.

South Carolina's costs sit meaningfully below both adjacent states: North Carolina averages $112 monthly, while Georgia averages $121. Within the Southeast region, only West Virginia posts lower costs at $87 monthly. The state falls in the region's low-cost tier alongside West Virginia, well below mid-tier states like North Carolina and Georgia, and far below high-cost markets like Florida ($144) and Maryland ($155). The $68 monthly gap between the region's cheapest and most expensive states reflects differences in legal climate, claims patterns, and market conditions.

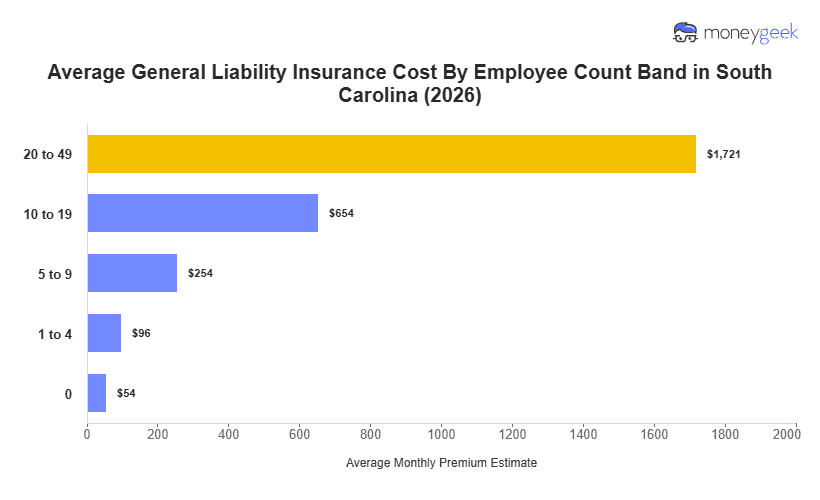

Use South Carolina's below-average position as a starting benchmark, but recognize that your actual cost depends on industry risk level, revenue exposure and claims history. These factors can move you significantly above or below the state average. To get a cost estimate based on your business profile, use the South Carolina general liability insurance cost calculator below.