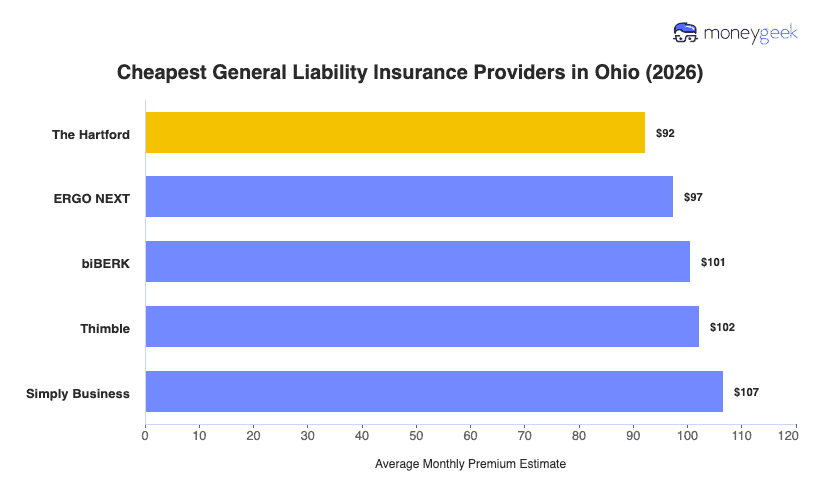

MoneyGeek analyzed general liability rates across 408 business types in Ohio from 10 major providers to identify which insurers most often deliver the lowest general liability rates for businesses with $1 million per occurrence/$2 million aggregate coverage.

- The Hartford: Most affordable for creative professionals and consulting services (photography, videography, IT consultants, virtual assistants)

- ERGO NEXT: Lowest rates for construction trades and personal services (concrete contractors, handyman services, massage therapy, tattoo shops)

- biBerk: Cheapest for cleaning services and fitness businesses (house cleaning, janitorial services, yoga studios, personal training)

- Thimble: Lowest rates for specialized construction and engineering (HVAC contractors, electrical contractors, engineering firms, excavation contractors)

- Simply Business: Most affordable for retail stores and tech services (book stores, gift shops, software development, web design)

[Click Each Provider To Learn More]

Your actual premium depends on your industry's risk profile, annual revenue, employee count, and where you operate in Ohio. A small manufacturer in Akron managing equipment risks faces different exposures than a landscaping contractor in Toledo dealing with lake-effect snow, or a food vendor at the Ohio State Fair. Request quotes that reflect your specific operations and the seasonal challenges Ohio businesses face.