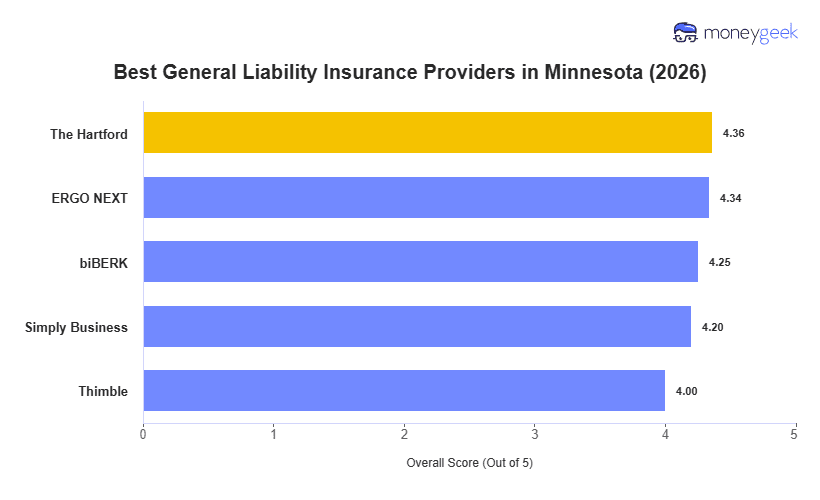

Not every insurer balances low rates with reliable claims service and flexible coverage. Of the 10 major providers we analyzed at $1 million per occurrence/$2 million aggregate limits across Minnesota, these five ranked as the best and most affordable for small businesses statewide:

- The Hartford: Best Overall, Best for Professional and Institutional Businesses

- ERGO NEXT: Best for Customer Experience

- biBerk: Best for Service Businesses (Especially With Physical Locations)

- Simply Business: Best for Tech and IT Businesses

- Thimble: Best for Short-Term and On-Demand Coverage

Whether you run a craft brewery in St. Paul or a snow removal service in Mankato, your risks shape which provider fits best. This table lays out rankings and rates to help you compare options side by side.