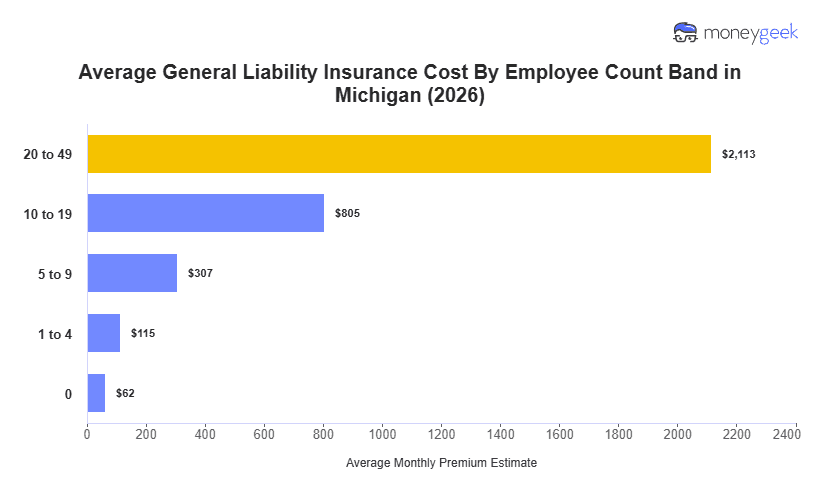

General liability insurance costs in Michigan average $115 per month, or $1,381 annually, for businesses with one to four employees. This sits 6% below the national average of $123 monthly. Michigan ranks 26th nationally for affordability, landing in the middle of the pack.

All three states bordering Michigan are cheaper: Indiana at $106 monthly, Wisconsin at $108 and Ohio at $110. These neighbors cluster tightly within a $4 range and rank more affordable nationally. Across the broader Midwest, Illinois breaks the pattern at $141 per month, 22% above Michigan and 46% over the national benchmark. This tight border-state grouping suggests Michigan sits just above a lower-cost Great Lakes tier but well below regional outliers.

Treat Michigan's average as orientation, not prediction. Two Michigan businesses can see very different premiums based on industry risk, business size and the coverage limits they select. These factors shift costs more than the state benchmark alone. A Michigan general liability insurance cost calculator is available below for a more personalized estimate.