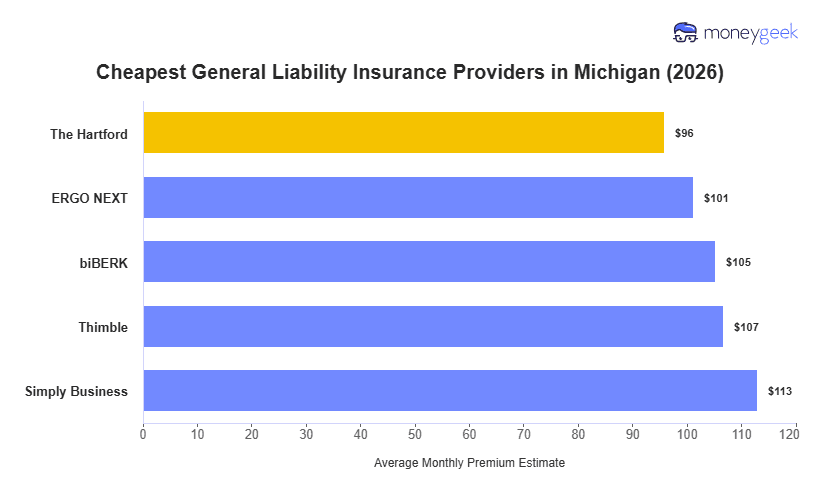

Michigan business owners looking for the cheapest general liability insurance can start by knowing which providers consistently offer the lowest rates for their type of operation. Our analysis of rates across 408 business types found these five providers consistently offer Michigan small businesses the lowest rates:

- The Hartford: Most affordable for professional services and creative businesses (IT consultants, accounting firms, photography, DJ services)

- ERGO NEXT: Lowest rates for hands-on trades and personal services (carpentry, roofing, hair salons, catering)

- biBERK: Cheapest for cleaning services and fitness businesses (house cleaning, janitorial services, gyms, yoga studios)

- Thimble: Most affordable for outdoor and specialty contractors (lawn care, tree service, painting contractors, plumbing contractors)

- Simply Business: Lowest rates for retail operations and food businesses (bookstores, gift shops, bakeries, daycare centers)

>> [Click Each Provider To Learn More]

Your actual rate depends on your specific industry, revenue, employee count and claims history, so a Grand Rapids contractor might pay differently than a Detroit retailer even with the same provider. Use these categories as a starting point, then compare quotes from multiple insurers to find your lowest price.