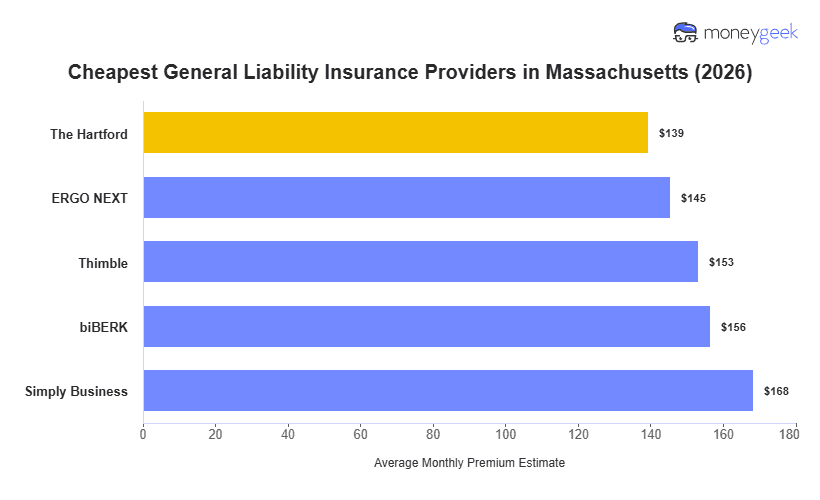

When comparing the general liability insurance companies in Massachusetts, a few insurers stand out for delivering the most affordable general liability coverage across different business types:

- The Hartford: Lowest rates for creative professionals and healthcare providers (photography, DJ services, massage therapy, holistic health practices)

- ERGO NEXT: Most affordable for hands-on trades and personal services (carpentry, HVAC contractors, beauty salons, estheticians)

- Thimble: Cheapest for heavy construction and specialty contractors (roofing contractors, electrical contractors, pest control, lawn care services)

- biBERK: Most affordable for cleaning services and fitness businesses (janitorial services, house cleaning, yoga studios, personal training)

>> [Click Each Provider To Learn More]

Your actual rate will vary based on your specific industry, business size, claims history and location within Massachusetts, so treat these findings as a starting point rather than a guaranteed price.