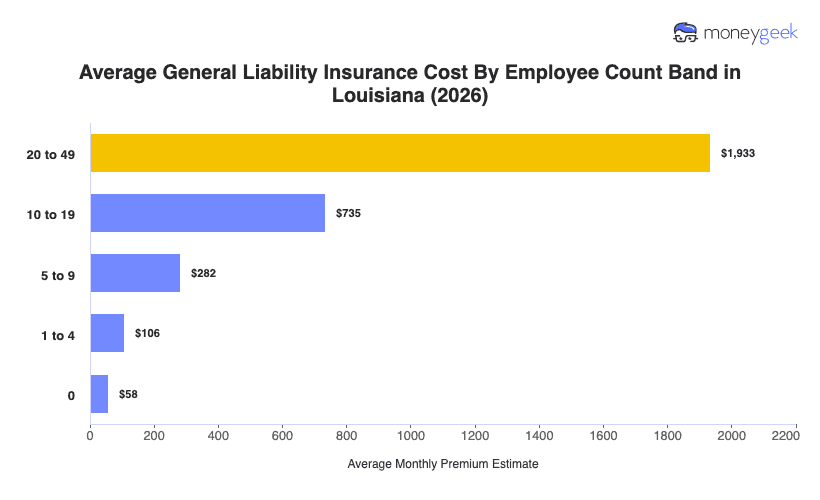

General liability costs in Louisiana average $106 monthly ($1,267 annually) for businesses with one to four employees carrying $1 million per occurrence/$2 million aggregate limits. This benchmark runs 15% below the national average of $123 monthly, placing Louisiana 17th most affordable among all states.

Border state comparisons show Louisiana in the middle tier. While several, like Mississippi and Arkansas are more affordable, Texas’ average premium exceeds Louisiana by $16. The spread reflects population density and commercial activity differences: Mississippi has the smallest business base, Louisiana sits mid-sized and Texas carries the highest claim volume.

Treat Louisiana’s state average as a reference point, not a quote. Your actual premium depends on industry claim exposure, operational risk profile and loss history, even when coverage limits match. A Louisiana general liability insurance cost calculator is available below for a more personalized estimate.