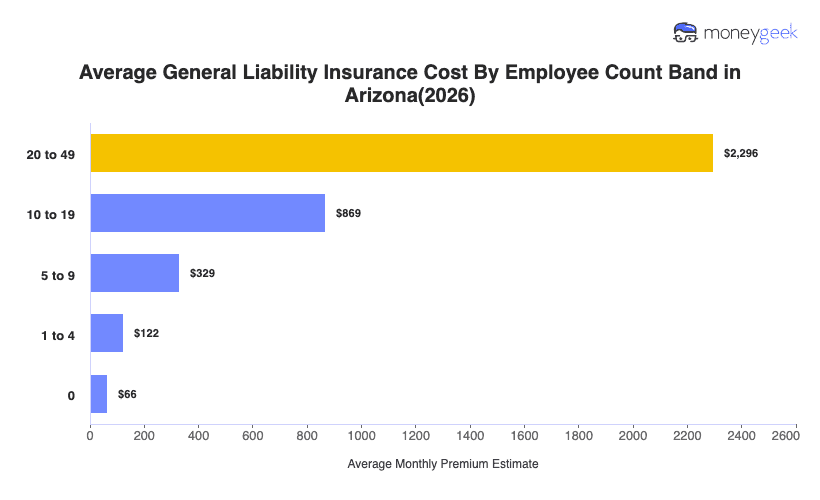

The cost of general liability insurance in Arizona averages $122 monthly ($1,470 annually) for businesses with one to four employees and limits of $1 million per occurrence (per claim)/$2 million aggregate (total). Running 0.3% lower than the national average of $123 monthly, Arizona ranks 30th nationally for affordability.

Arizona's costs fall between regional extremes. Small businesses in New Mexico and Utah, which share borders with Arizona, pay less at $102 and $110 per month. In comparison, general liability insurance in California costs 56% higher at $190 monthly.

This state average serves as a reference point, not a quote. Actual costs shift based on your industry's claim exposure, specific business operations and claims history, even when coverage limits remain the same. An Arizona general liability insurance cost calculator is available below for a more personalized estimate.