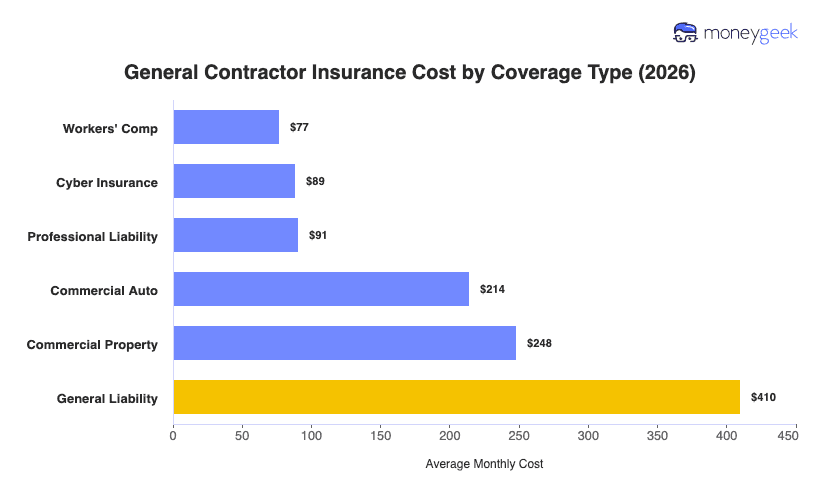

The average cost of business insurance for general contractors is $188 per month, or $2,256 per year, averaged across the six most common coverage types. That figure reflects businesses with one to four employees across all 50 states and Washington, D.C., modeled at standard policy limits of $1 million per occurrence and $2 million aggregate, with commercial auto sized across 16 vehicle types.

That average spans a wide range because your business carries several policies, each priced on different logic. Individual coverage costs run from $77 to $410 per month, and in our analysis, that $333 gap reflects two distinct pricing models. Workers' comp is payroll-rated, so your premium tracks what you pay your crew rather than how many jobs you run. General liability is exposure-rated, priced around the jobsite risk, completed operations and contract scope your business carries.

The table below breaks both down by coverage type. Use the figures as benchmarks, since your actual premiums depend on your trade, crew size and state.