No federal rule requires a plaintiff to disclose whether an outside investor is funding a lawsuit. For a small business responding to a claim, that blind spot can shape settlement outcomes without the defendant ever knowing it. The arrangement is called third-party litigation funding, or TPLF: investors with no connection to a legal dispute provide money to plaintiffs or law firms in exchange for a share of the proceeds.

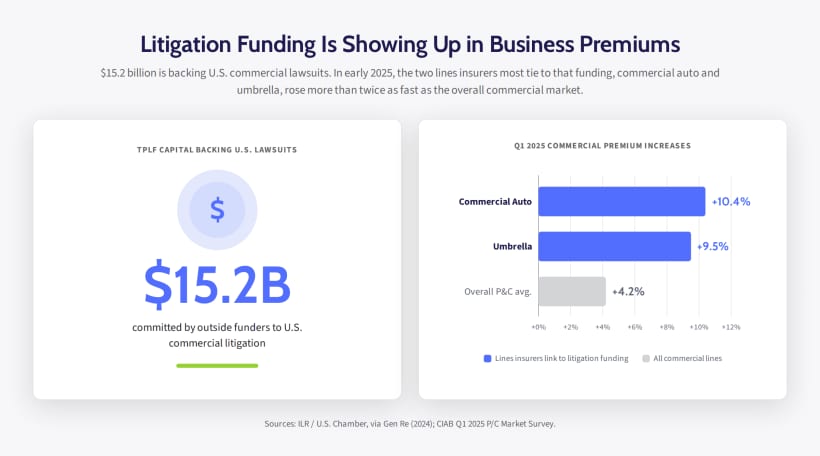

Commercial auto premiums rose 10.4% and umbrella premiums rose 9.5% in the first quarter of 2025, the two highest increases across all commercial lines, according to the Council of Insurance Agents and Brokers. Agents and brokers surveyed connected both increases to TPLF exposure. Even a business that is never sued can still pay for this trend through higher premiums, because insurers price TPLF-linked litigation risk into commercial lines across the board. Those 2025 pricing signals are already shaping small business insurance renewals heading into 2026.