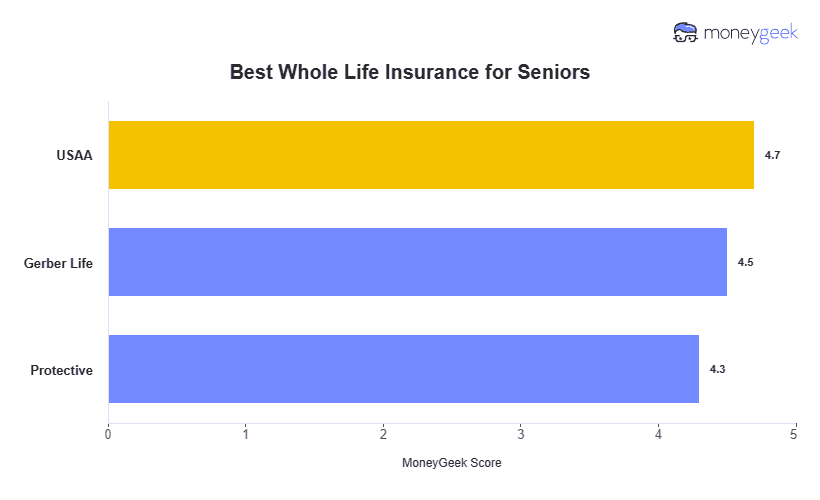

USAA is the best whole life insurance for seniors overall, with the highest issue age, high coverage limits and competitive rates. Gerber Life is the most affordable option for seniors ages 55 to 65, while Protective is best for senior smokers.

The rate gap between these three carriers widens sharply with age. At 60 years old, the spread between the cheapest and most expensive carrier in our analysis is $135 per month. By 70, that gap grows to $130 to $170, depending on gender. Purchasing coverage before 65 saves you the most over the life of your policy.