The average cost of home inspection business insurance runs $59 per month, or $713 per year, based on MoneyGeek's analysis of business insurance costs for home inspectors across six coverage types, 50 states plus DC and firms with one to four employees at standard $1 million per occurrence/$2 million aggregate limits.

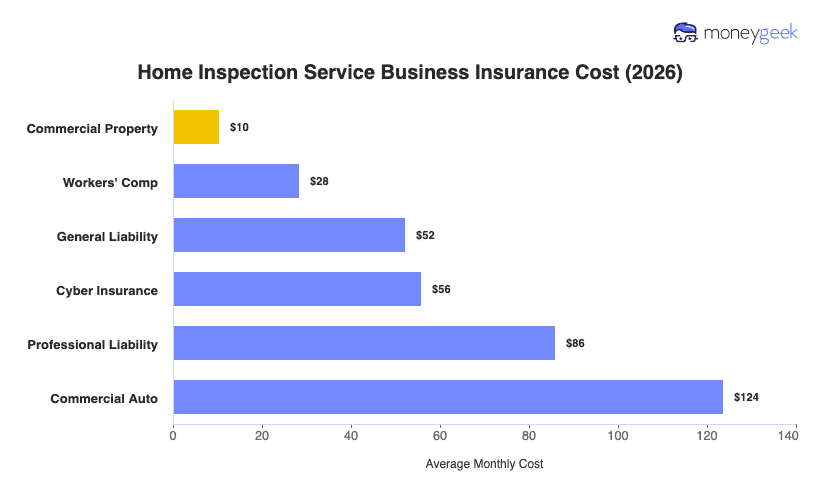

Individual coverage types range from $10 to $124 per month. Commercial property is the most affordable coverage type because most home inspection businesses operate from a vehicle or home office, so owned property exposure stays minimal. Commercial auto costs the most, so if you drive to every job, insurers price that road exposure into your rate. Within real estate and property services, home inspection is one of the more affordable industries, so if your quotes are running higher than these benchmarks, your specific risk profile is likely doing the work.

The figures in the table below are benchmarks, not quotes, and your actual premium reflects your specific business profile.