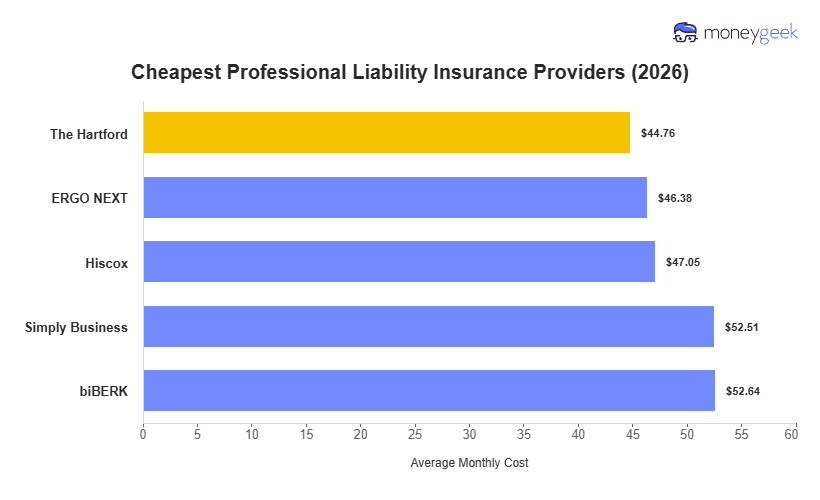

For most small businesses, our analysis found The Hartford is the cheapest professional liability insurance provider with rates that are 20% below the national average at $45/mo. The insurer also has close competitors including ERGO NEXT, Hiscox, Simply Business and biBERK for affordable coverage.

However, these companies are cheap for most companies with 1 to 4 employees, and your ideal professional liability insurance fit will depend on your small business's unique profile. So below, we've broken down each of our picks and who they are offer the lowest rates for:

- The Hartford: Most affordable for office-based, real estate and hospitality-related professional services (consultants, tech developers, financial services, travel agents).

- ERGO NEXT: Cheapest professional liability policies for high risk professions and B2C focused business areas (lawyers, security companies, construction/contracting, childcare, healthcare)

- Hiscox: Primarily the lowest cost for beauty and nonprofit services (estheticians, salons, social workers, animal rescues)

- Simply Business: You'll generally find the lowest professional liability rates if you're in the cleaning industry with Simply Business (janitorial services, carpet cleaning, chimney sweeps, junk removal)

- biBERK: If you're in a business area surrounding recreation and sports, biBERK is a very affordable provider for most businesses in this area (sports teams, fitness related clubs, dance studios)

Keep in mind that these companies should be used as a starting point rather than a final answer, and they may not have the lowest professional liability insurance costs once you get quotes.

In tech, real estate, media, advertising or financial services? These industries typically refer to this coverage as errors and omissions insurance. Our Cheapest E&O insurance guide covers the same top carriers framed for these industry areas.

Below you can compare each of these cheap insurers at a national level, side by side.