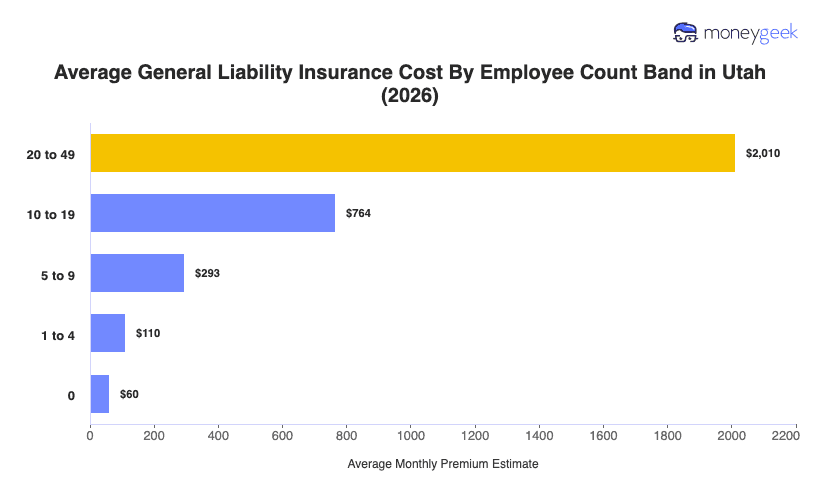

The average cost of general liability insurance in Utah is $110 per month ($1,319 per year) for most small businesses. That benchmark sits 11% below the national average of $123 per month ($1,474 per year).

Utah ranks 21st in affordability, placing it on the less-expensive side nationally. Neighboring-state benchmarks cover a wide range: Idaho averages $97 per month, while Arizona averages $122 and Colorado averages $146, with Utah falling between those reference points. States within the Mountain region average from $95 in Montana to $146 in Colorado per month, with Utah clustering in the lower-middle of that spread.

This state average is a benchmark, not a quote, as premiums can shift with industry exposure, revenue or payroll size, and coverage limits. As a checkpoint, Utah’s average helps you see whether you’re landing near the benchmark or meaningfully above it. Comparing the neighbor and regional ranges can also help identify which drivers explain most of the difference in your case, especially when operations or limits push costs toward the higher end.