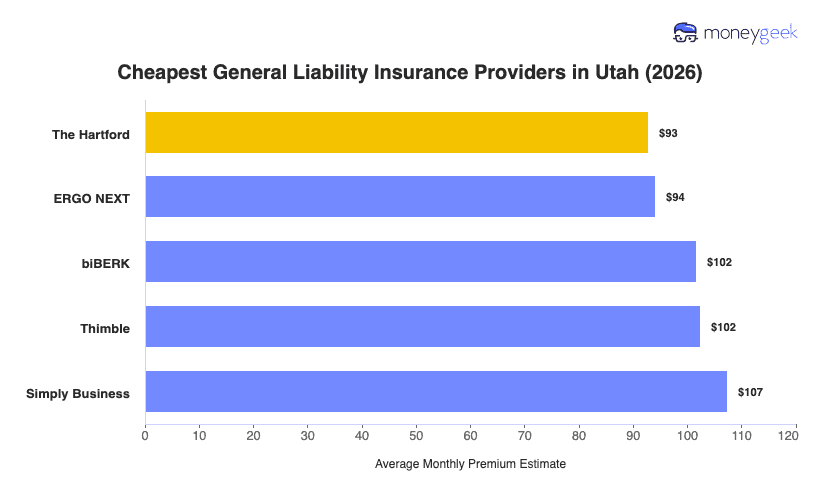

Finding the cheapest general liability insurance in Utah means knowing which providers consistently offer the lowest rates for businesses like yours. We analyzed rates across 408 business types and 10 major insurers for policies with $1 million per occurrence/$2 million aggregate limits and found these insurers offer the most affordable rates in the state:

- The Hartford: Most affordable for creative services and professional consulting (photography studios, art galleries, accounting firms, financial advisors)

- ERGO NEXT: Lowest rates for personal services and construction trades (barber shops, massage therapists, plumbing contractors, HVAC contractors)

- biBerk: Cheapest for cleaning services and fitness businesses (house cleaning, janitorial services, yoga studios, personal training)

- Simply Business: Most affordable for childcare providers and food retail (daycare centers, in-home daycares, bakeries, butcher shops)

[Click Each Provider To Learn More]

Your actual rate depends on your specific industry, revenue and claims history. Whether you're running a tech startup in Silicon Slopes or a construction firm working along the Wasatch Front, use these provider recommendations as your starting point for comparing quotes.