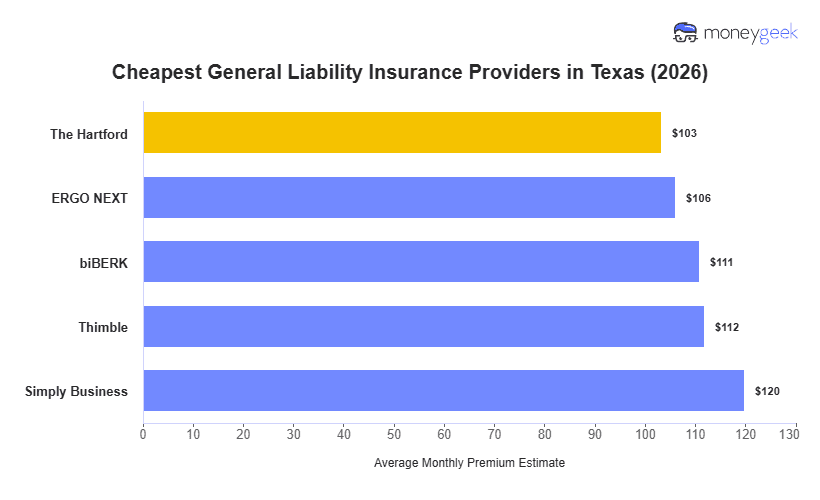

We analyzed general liability rates across 408 business types in Texas to identify which insurers most often deliver the lowest general liability rates for small businesses across the state. The following providers typically offer the best pricing in distinct business categories:

- The Hartford: Lowest rates for professional services and creative businesses (accounting firms, financial advisors, web development, photography, videography, art galleries)

- ERGO NEXT: Most affordable for hands-on services and customer-facing operations (beauty salons, dog grooming, mobile bartending, catering, handyman services, appliance repair)

- biBERK: Cheapest for active service businesses and wellness providers (house cleaning, personal training, yoga studios, veterinary practices)

- Thimble: Lowest rates for construction trades (electrical contractors, plumbing contractors, general contractors, drywall contractors)

>> Click each provider to learn more

These pricing patterns reflect where each insurer competes most aggressively in the Texas market, but your actual premium depends on factors like whether you operate in a major metro area like Houston or Dallas versus a smaller city, your specific trade risks and your claims history. Compare quotes from your top matches to find your lowest rate.