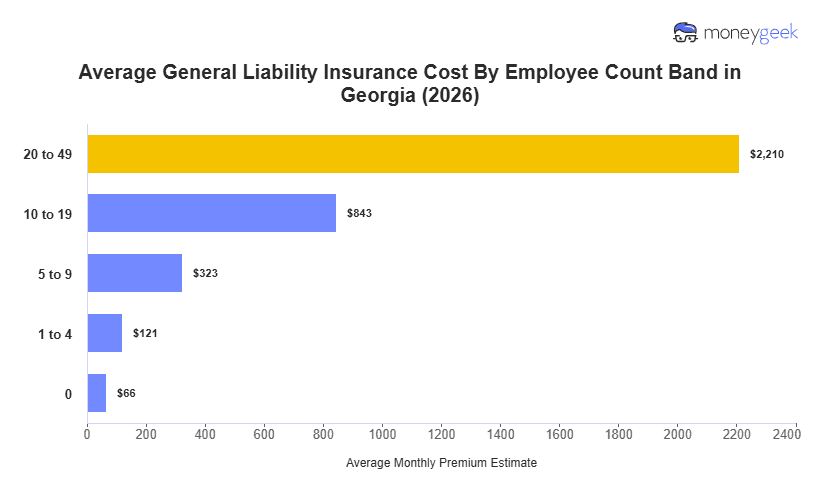

The cost of general liability insurance for Georgia businesses with one to four employees averages $121 monthly, or $1,451 annually, based on MoneyGeek's analysis of premium estimates from over 400 business types statewide. Georgia's rate is just $2 more per month, ranking it 27th for affordability among all states.

Adjacent states reveal distinct pricing patterns. Alabama businesses pay roughly $100 monthly, about $21 less than Georgia's benchmark, while North Carolina sits closer at $112. Florida, which also shares a border with Georgia, diverges substantially at $144 per month. A Warner Robins café owner budgeting $121 monthly would spend $144 across the state line in Jacksonville, which is an additional $276 annually for comparable coverage. Within the broader Southeast, costs range from South Carolina's $96 monthly average to Maryland's $155, positioning Georgia in the middle tier.

These figures represent aggregated estimates and don't predict individual quotes. An Atlanta roofing crew confronts different liability exposures than a Statesboro graphic design studio, which means actual premiums diverge based on industry classification, prior claims experience and selected policy limits. Use the state average to locate your business relative to the broader market, then identify which operational factors besides geography drive your specific premium. The Georgia general liability insurance cost calculator below provides an estimate based on your specific business inputs.