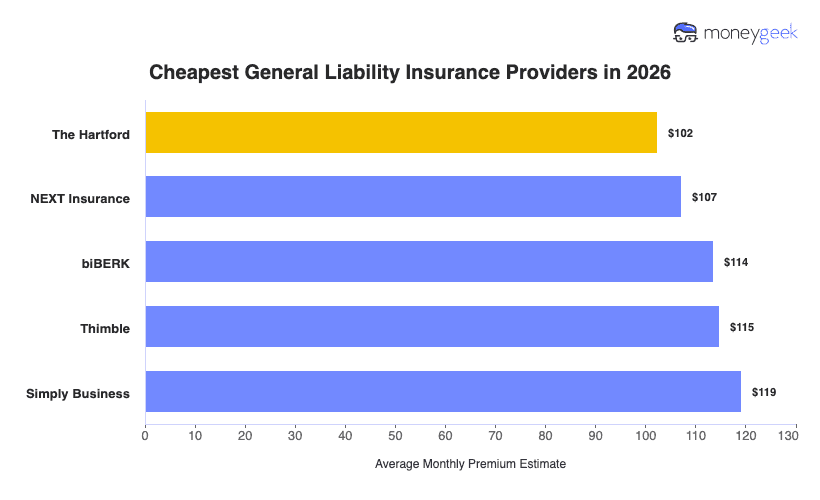

We found these providers to have the cheapest general liability insurance (AKA public liability insurance) on average:

- The Hartford : The cheapest general liability insurer overall with average rates of $102/mo which saves small businesses 17% on average. The company is generally cheapest for most professional service and office-based businesses (finance, tech, marketing)

- ERGO NEXT: NEXT saves businesses 13% on general liability insurance overall with average rates of $107/mo or $1,286/yr. The business insurer is cheapest for hands-on, operational service businesses (Contractors, Food & Beverage, Transportation)

- biBERK: biBERK rounds out our top three cheap general liability insurers with average savings of 8%. They are often cheapest for sole proprietor service businesses (cleaning, fitness, recreation).

>>(Click Each Provider To Learn More)

Your most affordable commercial general liability insurance provider and monthly rate can vary widely based on your specific business details. So, use these companies as a starting point for possible general liability policy costs, not a final answer.